Patrocinado

-

49 Publicações

-

1 fotos

-

0 Vídeos

-

Reside em pune

-

De pune

-

Female

-

07/02/1990

-

Seguido por 0 pessoas

Pesquisar

Atualizações Recentes

-

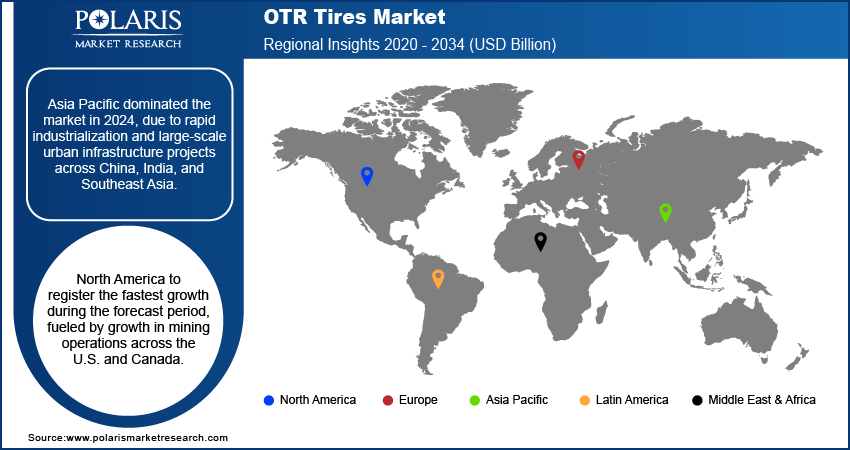

The global OTR tires market, valued at USD 3.37 billion in 2024, is projected to grow at a CAGR of 6.13% from 2025 to 2034. This growth is underpinned by the increasing demand for specialized tires across various industries, including construction, mining, agriculture, and industrial sectors. The market is segmented based on product type, end-user industry, and application, each exhibiting unique growth dynamics and opportunities.

In terms of product type, radial tires dominate the OTR tire market due to their superior performance characteristics, including better fuel efficiency, enhanced durability, and improved load-carrying capacity. Radial tires are particularly favored in applications requiring high-speed operations and long-distance travel. Bias tires, while offering cost advantages, are more suitable for applications involving lower speeds and shorter distances. The non-pneumatic tire segment is also gaining traction, driven by the need for maintenance-free and puncture-resistant tires in specific applications.

The end-user industry segment reveals that the construction sector holds a significant share of the OTR tire market. The increasing number of infrastructure development projects globally is driving the demand for construction equipment and, consequently, OTR tires. The mining industry follows closely, with the need for heavy-duty vehicles capable of operating in challenging terrains fueling the demand for specialized tires. The agriculture and industrial sectors also contribute to market growth, albeit at a slower pace.

Read More @ https://www.polarismarketresearch.com/industry-analysis/otr-tire-market

In terms of application, the earthmoving segment leads the OTR tire market, driven by the extensive use of earthmoving equipment in construction and mining operations. Loaders and dozers, graders, and material handling equipment also represent substantial shares of the market, each catering to specific operational requirements. The demand for tires in these applications is influenced by factors such as equipment utilization rates, operational hours, and terrain conditions.

The competitive landscape in the OTR tire market is marked by the presence of several key players focusing on product innovation and strategic collaborations. Companies are investing in research and development to enhance the performance and durability of their products, catering to the specific needs of various industries. Additionally, partnerships and collaborations with equipment manufacturers and fleet operators are enabling companies to expand their market reach and strengthen their product offerings.

Competitive Landscape:

• Bridgestone Corporation

• Michelin

• Continental AG

• Pirelli & C. S.p.A.

• The Yokohama Rubber Co., Ltd.

More Trending Latest Reports By Polaris Market Research:

Facility Management Market

Rainwear Market

Small Gas Engines Market

Extended Stay Hotel Market

Rainwear Market

Brain-Computer Interface (BCI) Gaming Market

Filtration and Drying Equipment Market

Aptamers Market

U.S. Distributed Fiber Optic Sensor Market

The global OTR tires market, valued at USD 3.37 billion in 2024, is projected to grow at a CAGR of 6.13% from 2025 to 2034. This growth is underpinned by the increasing demand for specialized tires across various industries, including construction, mining, agriculture, and industrial sectors. The market is segmented based on product type, end-user industry, and application, each exhibiting unique growth dynamics and opportunities. In terms of product type, radial tires dominate the OTR tire market due to their superior performance characteristics, including better fuel efficiency, enhanced durability, and improved load-carrying capacity. Radial tires are particularly favored in applications requiring high-speed operations and long-distance travel. Bias tires, while offering cost advantages, are more suitable for applications involving lower speeds and shorter distances. The non-pneumatic tire segment is also gaining traction, driven by the need for maintenance-free and puncture-resistant tires in specific applications. The end-user industry segment reveals that the construction sector holds a significant share of the OTR tire market. The increasing number of infrastructure development projects globally is driving the demand for construction equipment and, consequently, OTR tires. The mining industry follows closely, with the need for heavy-duty vehicles capable of operating in challenging terrains fueling the demand for specialized tires. The agriculture and industrial sectors also contribute to market growth, albeit at a slower pace. Read More @ https://www.polarismarketresearch.com/industry-analysis/otr-tire-market In terms of application, the earthmoving segment leads the OTR tire market, driven by the extensive use of earthmoving equipment in construction and mining operations. Loaders and dozers, graders, and material handling equipment also represent substantial shares of the market, each catering to specific operational requirements. The demand for tires in these applications is influenced by factors such as equipment utilization rates, operational hours, and terrain conditions. The competitive landscape in the OTR tire market is marked by the presence of several key players focusing on product innovation and strategic collaborations. Companies are investing in research and development to enhance the performance and durability of their products, catering to the specific needs of various industries. Additionally, partnerships and collaborations with equipment manufacturers and fleet operators are enabling companies to expand their market reach and strengthen their product offerings. Competitive Landscape: • Bridgestone Corporation • Michelin • Continental AG • Pirelli & C. S.p.A. • The Yokohama Rubber Co., Ltd. More Trending Latest Reports By Polaris Market Research: Facility Management Market Rainwear Market Small Gas Engines Market Extended Stay Hotel Market Rainwear Market Brain-Computer Interface (BCI) Gaming Market Filtration and Drying Equipment Market Aptamers Market U.S. Distributed Fiber Optic Sensor Market0 Comentários 0 Compartilhamentos 1K Visualizações 0 Anterior -

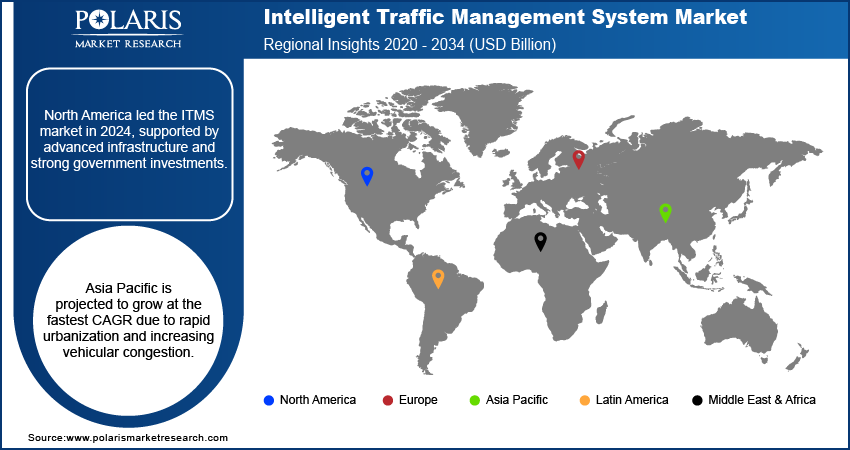

The global intelligent traffic management system market, valued at USD 12.15 billion in 2024, is anticipated to witness substantial growth, with a projected CAGR of 14.9% from 2025 to 2034. This growth is underpinned by the increasing demand for efficient traffic management solutions to address urban congestion, enhance road safety, and improve overall transportation efficiency. The market is segmented based on component, solution, and end-user, each exhibiting unique growth dynamics and opportunities.

In terms of components, traffic controllers and signals hold a significant share of the market. These systems are integral to managing traffic flow, reducing congestion, and ensuring the smooth movement of vehicles. The adoption of adaptive traffic signal control systems, which adjust signal timings based on real-time traffic conditions, is gaining traction. Additionally, the integration of video surveillance cameras and sensors is enhancing the monitoring and management of traffic, contributing to improved safety and efficiency.

From a solution perspective, traffic monitoring systems are leading the market. These systems provide real-time data on traffic conditions, enabling authorities to make informed decisions regarding traffic management. The implementation of intelligent driver information systems, which deliver timely updates to drivers about traffic conditions, road closures, and alternative routes, is also on the rise. These solutions are enhancing the driving experience and reducing travel time, thereby contributing to the overall efficiency of transportation networks.

Read More @ https://www.polarismarketresearch.com/industry-analysis/intelligent-traffic-management-system-market

The end-user segment is primarily dominated by government entities, including municipal corporations and transportation departments, which are investing in intelligent traffic management systems to address urban mobility challenges. Public-private partnerships are also emerging as a significant trend, facilitating the deployment of large-scale ITMS projects. The growing emphasis on sustainable urban mobility and the need for efficient public transportation systems are driving the adoption of intelligent traffic management solutions among public sector entities.

The competitive landscape is marked by the presence of several key players focusing on product innovation and strategic collaborations. Companies are investing in the development of scalable and integrated solutions that cater to the diverse needs of urban transportation systems. The emphasis on research and development is leading to the introduction of advanced technologies, such as AI and IoT, into traffic management systems, enhancing their capabilities and performance.

Competitive Landscape:

• Siemens Mobility

• Huawei Technologies

• Cisco Systems

• Thales Group

• IBM Corporation

More Trending Latest Reports By Polaris Market Research:

Medical Exoskeleton Market

Wood Protein Market

Video Management Software Market

Extended Stay Hotel Market

Wood Protein Market

HIV Diagnostics Market

Luxury Cigar Market

Veterinary Pain Management Market

Smoothies Market

The global intelligent traffic management system market, valued at USD 12.15 billion in 2024, is anticipated to witness substantial growth, with a projected CAGR of 14.9% from 2025 to 2034. This growth is underpinned by the increasing demand for efficient traffic management solutions to address urban congestion, enhance road safety, and improve overall transportation efficiency. The market is segmented based on component, solution, and end-user, each exhibiting unique growth dynamics and opportunities. In terms of components, traffic controllers and signals hold a significant share of the market. These systems are integral to managing traffic flow, reducing congestion, and ensuring the smooth movement of vehicles. The adoption of adaptive traffic signal control systems, which adjust signal timings based on real-time traffic conditions, is gaining traction. Additionally, the integration of video surveillance cameras and sensors is enhancing the monitoring and management of traffic, contributing to improved safety and efficiency. From a solution perspective, traffic monitoring systems are leading the market. These systems provide real-time data on traffic conditions, enabling authorities to make informed decisions regarding traffic management. The implementation of intelligent driver information systems, which deliver timely updates to drivers about traffic conditions, road closures, and alternative routes, is also on the rise. These solutions are enhancing the driving experience and reducing travel time, thereby contributing to the overall efficiency of transportation networks. Read More @ https://www.polarismarketresearch.com/industry-analysis/intelligent-traffic-management-system-market The end-user segment is primarily dominated by government entities, including municipal corporations and transportation departments, which are investing in intelligent traffic management systems to address urban mobility challenges. Public-private partnerships are also emerging as a significant trend, facilitating the deployment of large-scale ITMS projects. The growing emphasis on sustainable urban mobility and the need for efficient public transportation systems are driving the adoption of intelligent traffic management solutions among public sector entities. The competitive landscape is marked by the presence of several key players focusing on product innovation and strategic collaborations. Companies are investing in the development of scalable and integrated solutions that cater to the diverse needs of urban transportation systems. The emphasis on research and development is leading to the introduction of advanced technologies, such as AI and IoT, into traffic management systems, enhancing their capabilities and performance. Competitive Landscape: • Siemens Mobility • Huawei Technologies • Cisco Systems • Thales Group • IBM Corporation More Trending Latest Reports By Polaris Market Research: Medical Exoskeleton Market Wood Protein Market Video Management Software Market Extended Stay Hotel Market Wood Protein Market HIV Diagnostics Market Luxury Cigar Market Veterinary Pain Management Market Smoothies Market0 Comentários 0 Compartilhamentos 787 Visualizações 0 Anterior -

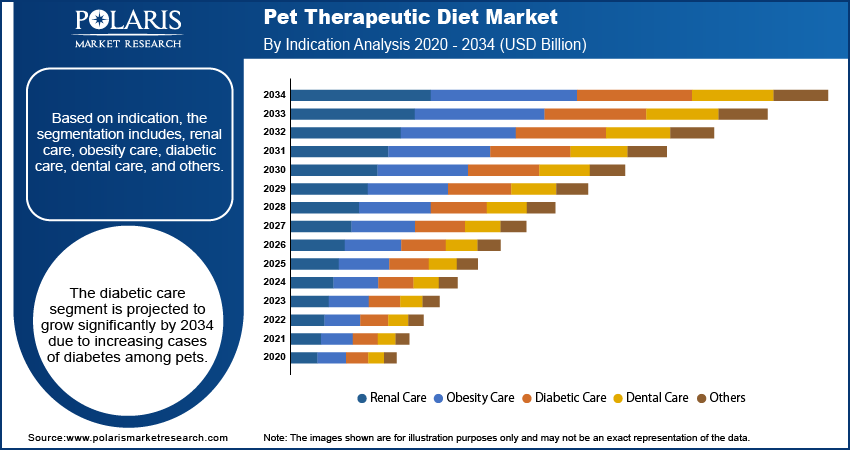

The global pet therapeutic diet market was valued at USD 2.36 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 7.22% from 2025 to 2034. This growth trajectory underscores the increasing prioritization of pet health and wellness, with owners seeking specialized nutritional solutions to manage chronic conditions such as obesity, diabetes, and renal disorders. The market's expansion is further fueled by the rising adoption of pets worldwide, particularly in regions like North America and Asia Pacific, where pet ownership is becoming more prevalent.

In North America, the pet therapeutic diet market is experiencing significant growth, driven by a combination of factors including increased pet ownership, heightened awareness of pet health, and the availability of a wide range of specialized dietary products. The United States, in particular, stands out as a major contributor to this growth, with the market valued at USD 1.84 billion in 2024. This expansion is supported by a robust distribution network encompassing veterinary clinics, pet specialty stores, and online platforms, facilitating easy access to therapeutic pet foods. Additionally, the growing trend of pet humanization, where pets are considered integral family members, is prompting owners to invest in high-quality, vet-recommended diets to ensure the well-being of their animals.

Conversely, the Asia Pacific region is emerging as the fastest-growing market for pet therapeutic diets. Countries such as China, India, and Japan are witnessing a surge in pet adoption, driven by urbanization, rising disposable incomes, and changing lifestyles that favor smaller living spaces conducive to pet ownership. This demographic shift is leading to an increased demand for specialized pet foods tailored to address specific health issues. Moreover, the expansion of e-commerce platforms is enhancing the accessibility of therapeutic diets, allowing pet owners in these regions to access a broader range of products. The market's growth in Asia Pacific is also supported by the increasing availability of locally manufactured therapeutic pet foods, which cater to regional preferences and dietary needs.

Read More @ https://www.polarismarketresearch.com/industry-analysis/pet-therapeutic-diet-market

The competitive landscape of the pet therapeutic diet market is characterized by the presence of several key players who are focusing on product innovation, strategic partnerships, and regional expansion to strengthen their market positions. These companies are investing in research and development to formulate diets that address a wide array of health conditions, thereby catering to the diverse needs of pets. Furthermore, the adoption of digital marketing strategies and the establishment of online sales channels are enabling these companies to reach a broader customer base, particularly in emerging markets where traditional retail infrastructure may be limited.

Competitive Landscape:

• Hill's Pet Nutrition

• Nestlé Purina Petcare

• Mars Petcare

• Royal Canin

More Trending Latest Reports By Polaris Market Research:

Omega 3 Supplements Market

String Wound Filter Materials Market

Green Hydrogen Market

HDPE Geogrid Market

String Wound Filter Materials Market

High-Performance Polyamides Market

Pulmonary Arterial Hypertension Market

Social and Emotional Learning Market

Low Rolling Resistance Tire Market

The global pet therapeutic diet market was valued at USD 2.36 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 7.22% from 2025 to 2034. This growth trajectory underscores the increasing prioritization of pet health and wellness, with owners seeking specialized nutritional solutions to manage chronic conditions such as obesity, diabetes, and renal disorders. The market's expansion is further fueled by the rising adoption of pets worldwide, particularly in regions like North America and Asia Pacific, where pet ownership is becoming more prevalent. In North America, the pet therapeutic diet market is experiencing significant growth, driven by a combination of factors including increased pet ownership, heightened awareness of pet health, and the availability of a wide range of specialized dietary products. The United States, in particular, stands out as a major contributor to this growth, with the market valued at USD 1.84 billion in 2024. This expansion is supported by a robust distribution network encompassing veterinary clinics, pet specialty stores, and online platforms, facilitating easy access to therapeutic pet foods. Additionally, the growing trend of pet humanization, where pets are considered integral family members, is prompting owners to invest in high-quality, vet-recommended diets to ensure the well-being of their animals. Conversely, the Asia Pacific region is emerging as the fastest-growing market for pet therapeutic diets. Countries such as China, India, and Japan are witnessing a surge in pet adoption, driven by urbanization, rising disposable incomes, and changing lifestyles that favor smaller living spaces conducive to pet ownership. This demographic shift is leading to an increased demand for specialized pet foods tailored to address specific health issues. Moreover, the expansion of e-commerce platforms is enhancing the accessibility of therapeutic diets, allowing pet owners in these regions to access a broader range of products. The market's growth in Asia Pacific is also supported by the increasing availability of locally manufactured therapeutic pet foods, which cater to regional preferences and dietary needs. Read More @ https://www.polarismarketresearch.com/industry-analysis/pet-therapeutic-diet-market The competitive landscape of the pet therapeutic diet market is characterized by the presence of several key players who are focusing on product innovation, strategic partnerships, and regional expansion to strengthen their market positions. These companies are investing in research and development to formulate diets that address a wide array of health conditions, thereby catering to the diverse needs of pets. Furthermore, the adoption of digital marketing strategies and the establishment of online sales channels are enabling these companies to reach a broader customer base, particularly in emerging markets where traditional retail infrastructure may be limited. Competitive Landscape: • Hill's Pet Nutrition • Nestlé Purina Petcare • Mars Petcare • Royal Canin More Trending Latest Reports By Polaris Market Research: Omega 3 Supplements Market String Wound Filter Materials Market Green Hydrogen Market HDPE Geogrid Market String Wound Filter Materials Market High-Performance Polyamides Market Pulmonary Arterial Hypertension Market Social and Emotional Learning Market Low Rolling Resistance Tire Market0 Comentários 0 Compartilhamentos 1K Visualizações 0 Anterior -

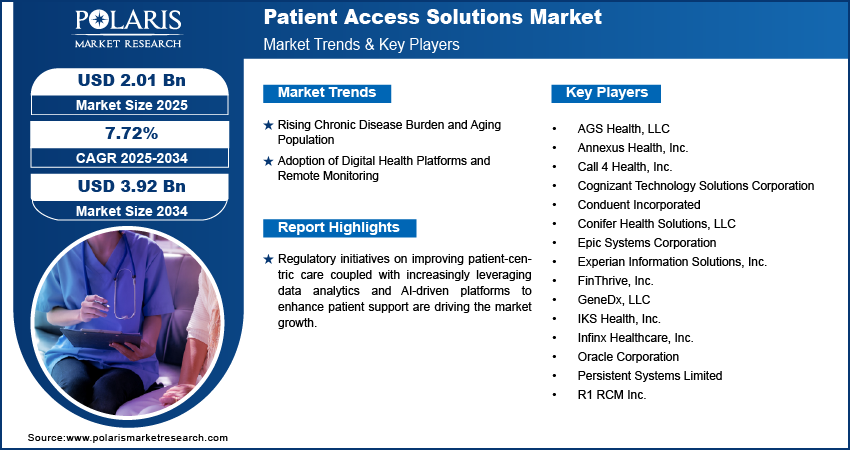

The global patient access solutions market size was valued at USD 1.87 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 7.72 % from 2025 through 2034. This growth trajectory reflects the increasing focus on end-to-end eligibility verification, claims denial management and patient registration efficiency across healthcare systems worldwide. Regional manufacturing trends in healthcare IT solutions, along with cross-border supply chains for software deployment and service delivery, are influencing how different geographies adopt and scale patient access platforms. In North America, established healthcare infrastructure, regulatory mandates on revenue cycle management and high digital-health penetration have accelerated market penetration strategies for leading vendors. Europe is characterised by strong data-protection frameworks (such as GDPR), multi-national reimbursement systems and cross-border service models that emphasise interoperability and service consolidation. Meanwhile, the Asia Pacific region is emerging as a high-growth zone, motivated by rising healthcare access, digital-health initiatives, and growing adoption of cloud-based patient access systems across diverse markets.

The primary driver across these regions is the escalating volume of healthcare claims, increasing complexity of payer rules and the resulting cost pressures on providers. For instance, healthcare organisations in North America report increasing claim denials and documentation overheads, which has spurred demand for robust patient access solutions that automate eligibility verification, payment estimation and prior authorisation workflows. In Europe, value-based care models and digital-first patient engagement strategies have triggered widespread adoption of patient access software and services. In Asia Pacific, the driver lies in rapid expansion of health insurance coverage, rising patient volume and improved hospital information systems, thereby creating a strong addressable market for both software and services. However, restraints persist: in many markets high upfront deployment cost, integration challenges with legacy systems and variable provider readiness slow roll-out and margin realisation. Moreover, in regions with limited connectivity or regulatory complexity, cross-border supply chains for service delivery can introduce latency and compliance risk.

Read More @ https://www.polarismarketresearch.com/industry-analysis/patient-access-solutions-market

Opportunities emerge regionally when providers adopt cloud-based and SaaS delivery models, enabling faster deployment, lower total cost of ownership and scalability across hospital networks. In North America, strategic partnerships between software vendors and large hospital systems offer opportunities to bundle patient access with broader revenue-cycle management platforms, thus improving value chain optimisation. In Europe, regional standardisation initiatives for healthcare data exchange provide opportunities for vendors to embed advanced analytics and interoperability features into their offerings. Asia Pacific presents a fertile setting for market penetration strategies targeting emerging healthcare providers, government-funded infrastructure development and digital-health adoption among private hospitals. Advances in mobile patient-engagement, AI-enabled front-end registration, and remote verification represent strong trends. The trend of shifting from on-premise to cloud-native deployment and serving mobile patients across geographies is a feature common across regions, reflecting increased focus on scalability, service models and rapid market entry.

In summation, regional differences will shape competitive dynamics in the global patient access solutions market. North America leads owing to scale and maturity, Europe emphasises regulatory-driven adoption and cross-border service models, and Asia Pacific offers the highest growth potential underpinned by expanding healthcare access and digital transformation. Vendors and investors alike should tailor regional manufacturing trends, supply-chain localisation and market-penetration strategies accordingly to capture value in this evolving market.

Competitive Landscape:

• Cerner Corporation

• McKesson Corporation

• Cognizant Technology Solutions

• Experian Plc.

• 3M Company

More Trending Latest Reports By Polaris Market Research:

Continuous Glucose Monitoring Device Market

Parental Control Software Market

Cosmetic Dentistry Market

HDPE Geogrid Market

Parental Control Software Market

HVAC Accessories Market

Myeloproliferative Disorders Treatment Market

Disinfection Robots Market

Low Rolling Resistance Tire Market

The global patient access solutions market size was valued at USD 1.87 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 7.72 % from 2025 through 2034. This growth trajectory reflects the increasing focus on end-to-end eligibility verification, claims denial management and patient registration efficiency across healthcare systems worldwide. Regional manufacturing trends in healthcare IT solutions, along with cross-border supply chains for software deployment and service delivery, are influencing how different geographies adopt and scale patient access platforms. In North America, established healthcare infrastructure, regulatory mandates on revenue cycle management and high digital-health penetration have accelerated market penetration strategies for leading vendors. Europe is characterised by strong data-protection frameworks (such as GDPR), multi-national reimbursement systems and cross-border service models that emphasise interoperability and service consolidation. Meanwhile, the Asia Pacific region is emerging as a high-growth zone, motivated by rising healthcare access, digital-health initiatives, and growing adoption of cloud-based patient access systems across diverse markets. The primary driver across these regions is the escalating volume of healthcare claims, increasing complexity of payer rules and the resulting cost pressures on providers. For instance, healthcare organisations in North America report increasing claim denials and documentation overheads, which has spurred demand for robust patient access solutions that automate eligibility verification, payment estimation and prior authorisation workflows. In Europe, value-based care models and digital-first patient engagement strategies have triggered widespread adoption of patient access software and services. In Asia Pacific, the driver lies in rapid expansion of health insurance coverage, rising patient volume and improved hospital information systems, thereby creating a strong addressable market for both software and services. However, restraints persist: in many markets high upfront deployment cost, integration challenges with legacy systems and variable provider readiness slow roll-out and margin realisation. Moreover, in regions with limited connectivity or regulatory complexity, cross-border supply chains for service delivery can introduce latency and compliance risk. Read More @ https://www.polarismarketresearch.com/industry-analysis/patient-access-solutions-market Opportunities emerge regionally when providers adopt cloud-based and SaaS delivery models, enabling faster deployment, lower total cost of ownership and scalability across hospital networks. In North America, strategic partnerships between software vendors and large hospital systems offer opportunities to bundle patient access with broader revenue-cycle management platforms, thus improving value chain optimisation. In Europe, regional standardisation initiatives for healthcare data exchange provide opportunities for vendors to embed advanced analytics and interoperability features into their offerings. Asia Pacific presents a fertile setting for market penetration strategies targeting emerging healthcare providers, government-funded infrastructure development and digital-health adoption among private hospitals. Advances in mobile patient-engagement, AI-enabled front-end registration, and remote verification represent strong trends. The trend of shifting from on-premise to cloud-native deployment and serving mobile patients across geographies is a feature common across regions, reflecting increased focus on scalability, service models and rapid market entry. In summation, regional differences will shape competitive dynamics in the global patient access solutions market. North America leads owing to scale and maturity, Europe emphasises regulatory-driven adoption and cross-border service models, and Asia Pacific offers the highest growth potential underpinned by expanding healthcare access and digital transformation. Vendors and investors alike should tailor regional manufacturing trends, supply-chain localisation and market-penetration strategies accordingly to capture value in this evolving market. Competitive Landscape: • Cerner Corporation • McKesson Corporation • Cognizant Technology Solutions • Experian Plc. • 3M Company More Trending Latest Reports By Polaris Market Research: Continuous Glucose Monitoring Device Market Parental Control Software Market Cosmetic Dentistry Market HDPE Geogrid Market Parental Control Software Market HVAC Accessories Market Myeloproliferative Disorders Treatment Market Disinfection Robots Market Low Rolling Resistance Tire Market0 Comentários 0 Compartilhamentos 789 Visualizações 0 Anterior -

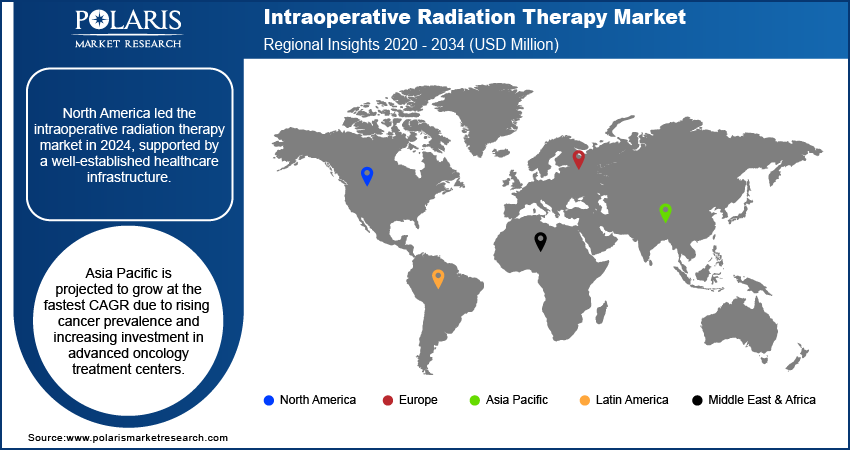

The global intraoperative radiation therapy (IORT) market, valued at USD 322.67 million in 2024, is projected to expand at a CAGR of 7.27% between 2025 and 2034, driven by regional advancements in oncological treatment systems, healthcare infrastructure modernization, and the growing prevalence of cancer worldwide. The steady rise in breast, colorectal, and pancreatic cancer cases—combined with technological innovations in radiation precision and dose management—continues to reinforce the market’s strategic relevance. As regional manufacturing trends and healthcare spending vary across North America, Europe, and Asia Pacific, the market’s structure is being increasingly shaped by policy frameworks, reimbursement dynamics, and the integration of clinical radiation solutions across tertiary healthcare centers.

In North America, the U.S. remains the primary revenue contributor, supported by advanced oncology treatment networks, strong reimbursement systems, and ongoing clinical trials sponsored by leading cancer centers. According to the National Cancer Institute, over 1.9 million new cancer cases were diagnosed in the U.S. in 2024, emphasizing the urgent need for localized and intraoperative radiation modalities. Hospitals across the region are accelerating adoption due to the ability of IORT to deliver concentrated radiation directly to tumor sites during surgery, reducing recurrence rates and shortening treatment cycles. Cross-border supply chains between the U.S. and Canada further strengthen equipment availability, while partnerships between device manufacturers and hospital systems have improved service penetration and clinical efficacy.

In Europe, strong regulatory support from the European Medicines Agency (EMA) and regional oncology consortiums has facilitated technology adoption across Germany, France, and the U.K. Germany, in particular, serves as a manufacturing hub for radiation oncology equipment, benefitting from domestic R&D incentives and regional export strength. The European cancer burden—projected to exceed 4 million new cases annually by 2030—continues to drive government funding and public-private partnerships aimed at modernizing cancer care. Regional manufacturers are expanding production facilities for mobile IORT systems, addressing demand for flexible, intra-surgical radiation procedures in both large hospital networks and specialized oncology centers.

Read More @ https://www.polarismarketresearch.com/industry-analysis/intraoperative-radiation-therapy-market

Meanwhile, Asia Pacific is emerging as the fastest-growing region, with healthcare modernization and rising awareness of precision oncology treatments driving robust adoption. China and India are implementing national cancer control programs emphasizing early detection and localized radiation therapy solutions. The World Health Organization’s regional data highlights an upward trajectory in cancer prevalence, particularly in breast and gynecological cancers, aligning with the region’s investment in advanced surgical radiotherapy equipment. Asia’s cross-border supply chains for medical devices are improving through increased local production and regulatory harmonization, making high-end IORT systems more accessible to secondary cities.

Overall, regional market penetration strategies now emphasize localized production, after-sales service infrastructure, and training for oncology specialists to maximize operational efficiency. Despite high capital costs and procedural complexity, global initiatives in healthcare digitization and government-led oncology programs continue to support steady market expansion. The convergence of radiation precision technologies, machine learning–assisted planning systems, and hybrid surgical radiotherapy units positions the IORT segment as a core pillar in the future of minimally invasive cancer care.

Competitive Landscape (major players):

• Zeiss Group

• IntraOp Medical Corporation

• iCAD Inc.

• Sordina IORT Technologies

• Eckert & Ziegler BEBIG

• GMV Innovating Solutions

More Trending Latest Reports By Polaris Market Research:

Cognitive Computing Market

Dental Fluoride Treatment Market

Brain Health Supplements Market

HDPE Geogrid Market

Dental Fluoride Treatment Market

Prestressed Concrete Wire and Strand Market

Tissue Clearing Market

Quantum Cryptography Market

Air Fryer Market

The global intraoperative radiation therapy (IORT) market, valued at USD 322.67 million in 2024, is projected to expand at a CAGR of 7.27% between 2025 and 2034, driven by regional advancements in oncological treatment systems, healthcare infrastructure modernization, and the growing prevalence of cancer worldwide. The steady rise in breast, colorectal, and pancreatic cancer cases—combined with technological innovations in radiation precision and dose management—continues to reinforce the market’s strategic relevance. As regional manufacturing trends and healthcare spending vary across North America, Europe, and Asia Pacific, the market’s structure is being increasingly shaped by policy frameworks, reimbursement dynamics, and the integration of clinical radiation solutions across tertiary healthcare centers. In North America, the U.S. remains the primary revenue contributor, supported by advanced oncology treatment networks, strong reimbursement systems, and ongoing clinical trials sponsored by leading cancer centers. According to the National Cancer Institute, over 1.9 million new cancer cases were diagnosed in the U.S. in 2024, emphasizing the urgent need for localized and intraoperative radiation modalities. Hospitals across the region are accelerating adoption due to the ability of IORT to deliver concentrated radiation directly to tumor sites during surgery, reducing recurrence rates and shortening treatment cycles. Cross-border supply chains between the U.S. and Canada further strengthen equipment availability, while partnerships between device manufacturers and hospital systems have improved service penetration and clinical efficacy. In Europe, strong regulatory support from the European Medicines Agency (EMA) and regional oncology consortiums has facilitated technology adoption across Germany, France, and the U.K. Germany, in particular, serves as a manufacturing hub for radiation oncology equipment, benefitting from domestic R&D incentives and regional export strength. The European cancer burden—projected to exceed 4 million new cases annually by 2030—continues to drive government funding and public-private partnerships aimed at modernizing cancer care. Regional manufacturers are expanding production facilities for mobile IORT systems, addressing demand for flexible, intra-surgical radiation procedures in both large hospital networks and specialized oncology centers. Read More @ https://www.polarismarketresearch.com/industry-analysis/intraoperative-radiation-therapy-market Meanwhile, Asia Pacific is emerging as the fastest-growing region, with healthcare modernization and rising awareness of precision oncology treatments driving robust adoption. China and India are implementing national cancer control programs emphasizing early detection and localized radiation therapy solutions. The World Health Organization’s regional data highlights an upward trajectory in cancer prevalence, particularly in breast and gynecological cancers, aligning with the region’s investment in advanced surgical radiotherapy equipment. Asia’s cross-border supply chains for medical devices are improving through increased local production and regulatory harmonization, making high-end IORT systems more accessible to secondary cities. Overall, regional market penetration strategies now emphasize localized production, after-sales service infrastructure, and training for oncology specialists to maximize operational efficiency. Despite high capital costs and procedural complexity, global initiatives in healthcare digitization and government-led oncology programs continue to support steady market expansion. The convergence of radiation precision technologies, machine learning–assisted planning systems, and hybrid surgical radiotherapy units positions the IORT segment as a core pillar in the future of minimally invasive cancer care. Competitive Landscape (major players): • Zeiss Group • IntraOp Medical Corporation • iCAD Inc. • Sordina IORT Technologies • Eckert & Ziegler BEBIG • GMV Innovating Solutions More Trending Latest Reports By Polaris Market Research: Cognitive Computing Market Dental Fluoride Treatment Market Brain Health Supplements Market HDPE Geogrid Market Dental Fluoride Treatment Market Prestressed Concrete Wire and Strand Market Tissue Clearing Market Quantum Cryptography Market Air Fryer Market0 Comentários 0 Compartilhamentos 1K Visualizações 0 Anterior -

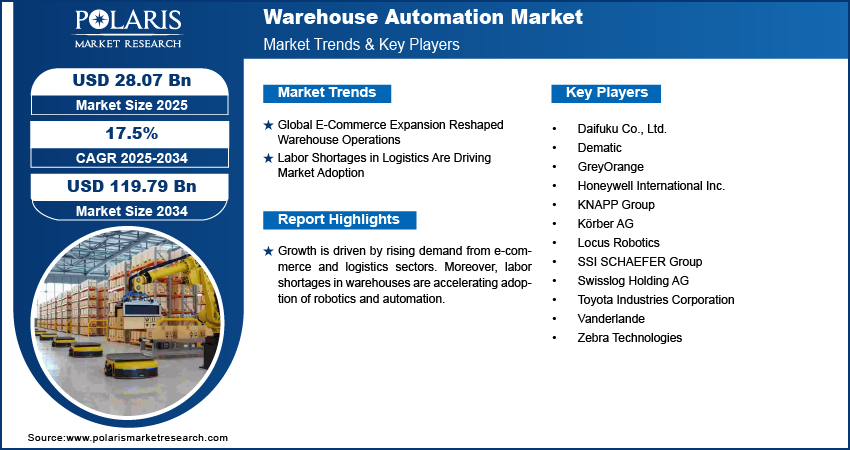

The global warehouse automation market, valued at USD 25.8 billion in 2024, is projected to expand at a CAGR of 17.5% from 2025 to 2034, driven by the convergence of robotics integration, digital logistics transformation, and the acceleration of e-commerce fulfillment technologies. Across industrial economies, regional manufacturing trends and cross-border supply chains are being reshaped by the automation imperative. As global trade flows rebalance post-pandemic, regions such as North America, Europe, and Asia Pacific have emerged as strategic epicenters for automation investments, each influenced by unique regulatory frameworks, industrial infrastructure, and technological adoption rates. In North America, the integration of advanced robotic handling systems and cloud-based inventory management is underpinned by the U.S. Department of Commerce’s support for smart manufacturing under the Manufacturing USA initiative. Europe’s strong regulatory alignment with Industry 5.0 standards—particularly in Germany, France, and the Netherlands—has reinforced sustainability-led warehouse modernization, while Asia Pacific’s rapid industrial digitalization, led by China, Japan, and South Korea, reflects a large-scale deployment of artificial intelligence–based logistics automation.

The market’s expansion is underwritten by a clear demand for efficiency in high-volume order processing and the transition toward data-driven inventory management systems. In the U.S. and Canada, warehouse automation penetration is expanding beyond e-commerce and into retail, pharmaceuticals, and automotive distribution. Europe, led by Germany’s industrial robotics base and the UK’s logistics innovation ecosystem, has seen significant adoption of automated guided vehicles (AGVs) and automated storage and retrieval systems (ASRS). Meanwhile, Asia Pacific remains the most dynamic region, with over 40% of new global warehouse construction incorporating automation elements, supported by China’s “Made in China 2025” policy framework and India’s rapid rise as a logistics hub under the PM Gati Shakti initiative. The regional competitive environment is further influenced by localized manufacturing bases for automation hardware, enabling faster customization and integration across verticals.

Drivers, Restraints, Opportunities, and Trends (DROS) define the regionally differentiated growth path of this market. The principal driver across all regions remains labor optimization—particularly in markets with tight labor availability and rising wage costs. According to the U.S. Bureau of Labor Statistics, logistics sector employment has grown 8.2% annually since 2020, intensifying demand for robotic assistance to sustain throughput levels. In Europe, energy efficiency regulations and carbon-neutral targets have driven warehouses to replace manual equipment with sensor-enabled, low-energy automation systems. In Asia Pacific, opportunities arise from large-scale infrastructure modernization and expanding cross-border trade corridors, which require harmonized, technology-enabled warehousing to manage throughput efficiency. However, challenges persist, particularly in regions where legacy infrastructure limits automation retrofits. Cost-intensive installation and limited interoperability between systems continue to constrain adoption in developing economies. Despite this, ongoing advancements in modular automation, AI-based route optimization, and 5G-enabled real-time tracking are mitigating cost barriers and enhancing integration capacity across global operations.

Regionally, North America dominates market share in terms of automation intensity per warehouse, while Asia Pacific is expected to lead in total deployment volume by 2030 due to high industrial growth rates and favorable policy support. Europe continues to invest heavily in robotic logistics through public–private partnerships under the Horizon Europe funding framework, encouraging sustainable automation practices. The intersection of digital logistics solutions, robotics engineering, and AI-based process control is reinforcing regional competitiveness across all three continents. The trend toward distributed warehousing and micro-fulfillment centers, particularly in North America and Asia Pacific, is reshaping warehouse design standards. This decentralization trend not only supports same-day delivery models but also creates sustained demand for compact automation modules capable of operating in smaller spaces.

Read More @ https://www.polarismarketresearch.com/industry-analysis/warehouse-automation-market

The global warehouse automation market, valued at USD 25.8 billion in 2024, is projected to expand at a CAGR of 17.5% from 2025 to 2034, driven by the convergence of robotics integration, digital logistics transformation, and the acceleration of e-commerce fulfillment technologies. Across industrial economies, regional manufacturing trends and cross-border supply chains are being reshaped by the automation imperative. As global trade flows rebalance post-pandemic, regions such as North America, Europe, and Asia Pacific have emerged as strategic epicenters for automation investments, each influenced by unique regulatory frameworks, industrial infrastructure, and technological adoption rates. In North America, the integration of advanced robotic handling systems and cloud-based inventory management is underpinned by the U.S. Department of Commerce’s support for smart manufacturing under the Manufacturing USA initiative. Europe’s strong regulatory alignment with Industry 5.0 standards—particularly in Germany, France, and the Netherlands—has reinforced sustainability-led warehouse modernization, while Asia Pacific’s rapid industrial digitalization, led by China, Japan, and South Korea, reflects a large-scale deployment of artificial intelligence–based logistics automation. The market’s expansion is underwritten by a clear demand for efficiency in high-volume order processing and the transition toward data-driven inventory management systems. In the U.S. and Canada, warehouse automation penetration is expanding beyond e-commerce and into retail, pharmaceuticals, and automotive distribution. Europe, led by Germany’s industrial robotics base and the UK’s logistics innovation ecosystem, has seen significant adoption of automated guided vehicles (AGVs) and automated storage and retrieval systems (ASRS). Meanwhile, Asia Pacific remains the most dynamic region, with over 40% of new global warehouse construction incorporating automation elements, supported by China’s “Made in China 2025” policy framework and India’s rapid rise as a logistics hub under the PM Gati Shakti initiative. The regional competitive environment is further influenced by localized manufacturing bases for automation hardware, enabling faster customization and integration across verticals. Drivers, Restraints, Opportunities, and Trends (DROS) define the regionally differentiated growth path of this market. The principal driver across all regions remains labor optimization—particularly in markets with tight labor availability and rising wage costs. According to the U.S. Bureau of Labor Statistics, logistics sector employment has grown 8.2% annually since 2020, intensifying demand for robotic assistance to sustain throughput levels. In Europe, energy efficiency regulations and carbon-neutral targets have driven warehouses to replace manual equipment with sensor-enabled, low-energy automation systems. In Asia Pacific, opportunities arise from large-scale infrastructure modernization and expanding cross-border trade corridors, which require harmonized, technology-enabled warehousing to manage throughput efficiency. However, challenges persist, particularly in regions where legacy infrastructure limits automation retrofits. Cost-intensive installation and limited interoperability between systems continue to constrain adoption in developing economies. Despite this, ongoing advancements in modular automation, AI-based route optimization, and 5G-enabled real-time tracking are mitigating cost barriers and enhancing integration capacity across global operations. Regionally, North America dominates market share in terms of automation intensity per warehouse, while Asia Pacific is expected to lead in total deployment volume by 2030 due to high industrial growth rates and favorable policy support. Europe continues to invest heavily in robotic logistics through public–private partnerships under the Horizon Europe funding framework, encouraging sustainable automation practices. The intersection of digital logistics solutions, robotics engineering, and AI-based process control is reinforcing regional competitiveness across all three continents. The trend toward distributed warehousing and micro-fulfillment centers, particularly in North America and Asia Pacific, is reshaping warehouse design standards. This decentralization trend not only supports same-day delivery models but also creates sustained demand for compact automation modules capable of operating in smaller spaces. Read More @ https://www.polarismarketresearch.com/industry-analysis/warehouse-automation-market0 Comentários 0 Compartilhamentos 948 Visualizações 0 Anterior -

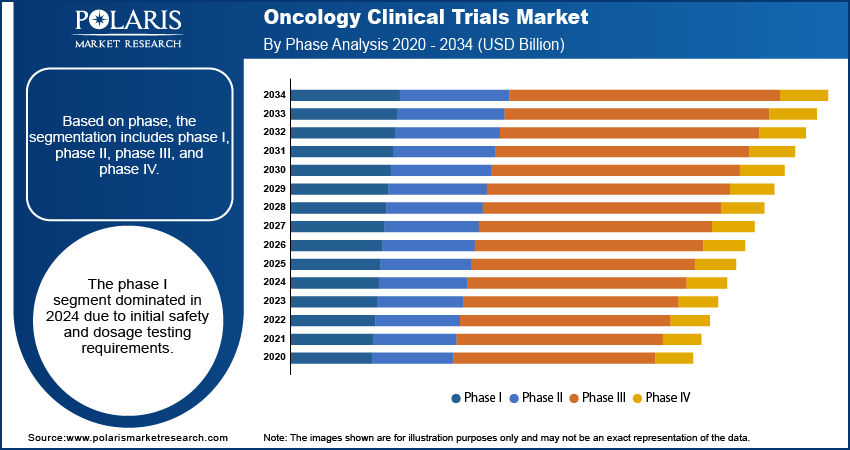

The oncology clinical trials market was valued at USD 14.21 billion in 2024 and is projected to expand at a CAGR of 5.17% between 2025 and 2034. Growth is increasingly defined by segmentation performance across trial phase (Phase I, II, III, IV), study design (interventional, observational), tumour indication (lung, breast, colorectal, hematologic) and sponsor type (pharma/biotech, academic, government). Within this framework, product differentiation is gaining significant traction: for example, cell- and gene-therapy oncology trials are a high-growth sub-segment, attracting premium pricing and specialised site infrastructure. In application-specific growth contexts such as immuno-oncology and precision-medicine trials, sponsors are leaning heavily on biomarker selection, decentralised monitoring and adaptive-design protocols which increase operational complexity but raise value-capture potential.

Drivers in the segmentation domain include the rising adoption of advanced therapeutics that mandate rigorous late-phase validation, thereby increasing volumes in Phase III and IV segments. The growth of companion diagnostic-linked oncology trials also reinforces product differentiation: trials tied to specific biomarkers or targeted therapies command higher investment and yield stronger returns. On the flip side, segmentation-specific restraints include the elevated cost and complexity of later-phase trials, as well as increased protocol burden for observational or real-world-evidence extensions which may reduce sponsor appetite. Additionally, smaller niche tumour indications can face recruitment limitations, limiting scale economies despite high value per patient. Opportunities lie in value-chain optimisation: sponsors can reduce cost per enrolment through centralised monitoring, remote patient engagement, and data-platform integration while targeting underserved indications where competition is lower and differentiated endpoints can justify premium trial pricing. Trends include the move away from traditional large-cohort interventional trials toward hybrid models combining observational follow-up, real-world-data, digital biomarkers and decentralised site networks; segment-wise performance increasingly favours trials with modular, patient-centric designs and adaptive-endpoints, and the demand for precision-medicine oncology trials is reshaping resource allocation across the value chain.

Read More @ https://www.polarismarketresearch.com/industry-analysis/oncology-clinical-trials-market

As the oncology clinical trials market evolves, sponsors must evaluate segmentation strategy rather than treat the market as monolithic: focusing on indications with strong unmet need, leveraging adaptive-design or decentralised models, and optimising trial-site configuration for cost efficiency. Value chain optimisation—via advanced analytics, digital-platform integration and patient-centric recruitment—is increasingly a source of competitive differentiation. The competitive industry landscape, highlighting top market holders in the segmentation-driven space, includes:

• IQVIA Inc.

• ICON plc

• Parexel International Corporation

• Syneos Health

• Labcorp Drug Development

More Trending Latest Reports By Polaris Market Research:

Blood Transfusion Diagnostics Market

Weatherstrip Seal Market

Electric Ship Market

HDPE Geogrid Market

Weatherstrip Seal Market

Micro Computed Tomography Market

Communication Based Train Control System Market

CBRN Defense Market

Tissue Paper Market

The oncology clinical trials market was valued at USD 14.21 billion in 2024 and is projected to expand at a CAGR of 5.17% between 2025 and 2034. Growth is increasingly defined by segmentation performance across trial phase (Phase I, II, III, IV), study design (interventional, observational), tumour indication (lung, breast, colorectal, hematologic) and sponsor type (pharma/biotech, academic, government). Within this framework, product differentiation is gaining significant traction: for example, cell- and gene-therapy oncology trials are a high-growth sub-segment, attracting premium pricing and specialised site infrastructure. In application-specific growth contexts such as immuno-oncology and precision-medicine trials, sponsors are leaning heavily on biomarker selection, decentralised monitoring and adaptive-design protocols which increase operational complexity but raise value-capture potential. Drivers in the segmentation domain include the rising adoption of advanced therapeutics that mandate rigorous late-phase validation, thereby increasing volumes in Phase III and IV segments. The growth of companion diagnostic-linked oncology trials also reinforces product differentiation: trials tied to specific biomarkers or targeted therapies command higher investment and yield stronger returns. On the flip side, segmentation-specific restraints include the elevated cost and complexity of later-phase trials, as well as increased protocol burden for observational or real-world-evidence extensions which may reduce sponsor appetite. Additionally, smaller niche tumour indications can face recruitment limitations, limiting scale economies despite high value per patient. Opportunities lie in value-chain optimisation: sponsors can reduce cost per enrolment through centralised monitoring, remote patient engagement, and data-platform integration while targeting underserved indications where competition is lower and differentiated endpoints can justify premium trial pricing. Trends include the move away from traditional large-cohort interventional trials toward hybrid models combining observational follow-up, real-world-data, digital biomarkers and decentralised site networks; segment-wise performance increasingly favours trials with modular, patient-centric designs and adaptive-endpoints, and the demand for precision-medicine oncology trials is reshaping resource allocation across the value chain. Read More @ https://www.polarismarketresearch.com/industry-analysis/oncology-clinical-trials-market As the oncology clinical trials market evolves, sponsors must evaluate segmentation strategy rather than treat the market as monolithic: focusing on indications with strong unmet need, leveraging adaptive-design or decentralised models, and optimising trial-site configuration for cost efficiency. Value chain optimisation—via advanced analytics, digital-platform integration and patient-centric recruitment—is increasingly a source of competitive differentiation. The competitive industry landscape, highlighting top market holders in the segmentation-driven space, includes: • IQVIA Inc. • ICON plc • Parexel International Corporation • Syneos Health • Labcorp Drug Development More Trending Latest Reports By Polaris Market Research: Blood Transfusion Diagnostics Market Weatherstrip Seal Market Electric Ship Market HDPE Geogrid Market Weatherstrip Seal Market Micro Computed Tomography Market Communication Based Train Control System Market CBRN Defense Market Tissue Paper Market0 Comentários 0 Compartilhamentos 880 Visualizações 0 Anterior -

The global drinking water adsorbents market size was valued at USD 3.47 billion in 2024 and is expected to grow at a compound annual growth rate (CAGR) of 4.4% from 2025 through 2034. This growth is underpinned by robust application-specific growth in municipal water treatment, industrial water systems and residential point-of-use (POU) filtration, and by product differentiation among adsorbent types such as activated carbon, zeolite, alumina, and specialised metal-oxide media. In the product-type dimension one sees activated carbon continuing to hold a dominant share due to its versatility in removing organics, taste and odor, yet segments such as engineered zeolites, manganese oxide media and nano-adsorbents are accelerating with differentiated performance for heavy metals, fluorides and emerging micropollutants. In the end-use application dimension, municipal water treatment remains the largest user segment, but value chain optimisation efforts are shifting focus toward industrial and POU/POE (point-of-entry) systems where adsorption media offer modular, scalable solutions. Segment-wise performance now hinges on service life, regeneration capability, cost per volume treated and footprint efficiency, driving manufacturers to tailor product and application portfolios accordingly.

Drivers of segmentation-driven growth include rapidly evolving contaminant profiles in water supplies—such as PFAS, microplastics and antibiotic-resistance genes—and the need for higher performance adsorbents which deliver on selectivity, regeneration and long life. This creates strong incentives for product differentiation: for instance, new adsorbents tailored to remove specific micropollutants at low concentrations are winning specification in industrial and municipal tenders. On the other hand, restraints include higher unit cost of advanced adsorbents compared to legacy carbon media, and fragmentation of the POU market which imposes high distribution and service costs. Further, certain segments face substitution risk from technologies such as reverse osmosis or ion-exchange, which may limit uptake of adsorbents unless clear value benefit is demonstrated.

Read More @ https://www.polarismarketresearch.com/industry-analysis/drinking-water-adsorbents-market

Opportunities surface in segments with rising regulatory pressure or emerging economies where infrastructure remains under-developed. For example, in industrial water treatment, adsorbents that reduce fouling of membranes or extend their life offer value-chain optimisation benefits. In POU systems, compact high-capacity media enable cost-effective home-filtration devices, representing a high-margin segment. Also, the combination of hybrid systems—adsorbents plus membranes or UV—presents growth niches. Trends include increasing integration of real-time monitoring of adsorbent bed life, smart sensor feedback, and the rise of regenerable media reflecting lifecycle cost consciousness. Another trend is the shift from commodity granular media to custom extruded or impregnated media designed for specific contaminant profiles and footprint constraints, thereby enabling application-specific growth pathways.

To summarise, the segmentation landscape in the global drinking water adsorbents market is evolving rapidly: product differentiation among adsorbent types, application-specific growth across municipal, industrial and residential domains, and value-chain optimisation through smarter media design are key to capturing the projected growth. Leading players positioning high-performance portfolio strategies include:

• Dow Chemical Company

• DuPont

• BASF SE

• KMI Zeolite

• Kuraray Co., Ltd.

More Trending Latest Reports By Polaris Market Research:

Aluminum Curtain Wall Market

Contract Cleaning Services Market

Natural Food Colors Market

HDPE Geogrid Market

Contract Cleaning Services Market

AI-Powered Enterprise Automation Market

Donkey Milk Market

Ophthalmic Drugs Market

Podcasting Market

The global drinking water adsorbents market size was valued at USD 3.47 billion in 2024 and is expected to grow at a compound annual growth rate (CAGR) of 4.4% from 2025 through 2034. This growth is underpinned by robust application-specific growth in municipal water treatment, industrial water systems and residential point-of-use (POU) filtration, and by product differentiation among adsorbent types such as activated carbon, zeolite, alumina, and specialised metal-oxide media. In the product-type dimension one sees activated carbon continuing to hold a dominant share due to its versatility in removing organics, taste and odor, yet segments such as engineered zeolites, manganese oxide media and nano-adsorbents are accelerating with differentiated performance for heavy metals, fluorides and emerging micropollutants. In the end-use application dimension, municipal water treatment remains the largest user segment, but value chain optimisation efforts are shifting focus toward industrial and POU/POE (point-of-entry) systems where adsorption media offer modular, scalable solutions. Segment-wise performance now hinges on service life, regeneration capability, cost per volume treated and footprint efficiency, driving manufacturers to tailor product and application portfolios accordingly. Drivers of segmentation-driven growth include rapidly evolving contaminant profiles in water supplies—such as PFAS, microplastics and antibiotic-resistance genes—and the need for higher performance adsorbents which deliver on selectivity, regeneration and long life. This creates strong incentives for product differentiation: for instance, new adsorbents tailored to remove specific micropollutants at low concentrations are winning specification in industrial and municipal tenders. On the other hand, restraints include higher unit cost of advanced adsorbents compared to legacy carbon media, and fragmentation of the POU market which imposes high distribution and service costs. Further, certain segments face substitution risk from technologies such as reverse osmosis or ion-exchange, which may limit uptake of adsorbents unless clear value benefit is demonstrated. Read More @ https://www.polarismarketresearch.com/industry-analysis/drinking-water-adsorbents-market Opportunities surface in segments with rising regulatory pressure or emerging economies where infrastructure remains under-developed. For example, in industrial water treatment, adsorbents that reduce fouling of membranes or extend their life offer value-chain optimisation benefits. In POU systems, compact high-capacity media enable cost-effective home-filtration devices, representing a high-margin segment. Also, the combination of hybrid systems—adsorbents plus membranes or UV—presents growth niches. Trends include increasing integration of real-time monitoring of adsorbent bed life, smart sensor feedback, and the rise of regenerable media reflecting lifecycle cost consciousness. Another trend is the shift from commodity granular media to custom extruded or impregnated media designed for specific contaminant profiles and footprint constraints, thereby enabling application-specific growth pathways. To summarise, the segmentation landscape in the global drinking water adsorbents market is evolving rapidly: product differentiation among adsorbent types, application-specific growth across municipal, industrial and residential domains, and value-chain optimisation through smarter media design are key to capturing the projected growth. Leading players positioning high-performance portfolio strategies include: • Dow Chemical Company • DuPont • BASF SE • KMI Zeolite • Kuraray Co., Ltd. More Trending Latest Reports By Polaris Market Research: Aluminum Curtain Wall Market Contract Cleaning Services Market Natural Food Colors Market HDPE Geogrid Market Contract Cleaning Services Market AI-Powered Enterprise Automation Market Donkey Milk Market Ophthalmic Drugs Market Podcasting Market0 Comentários 0 Compartilhamentos 958 Visualizações 0 Anterior -

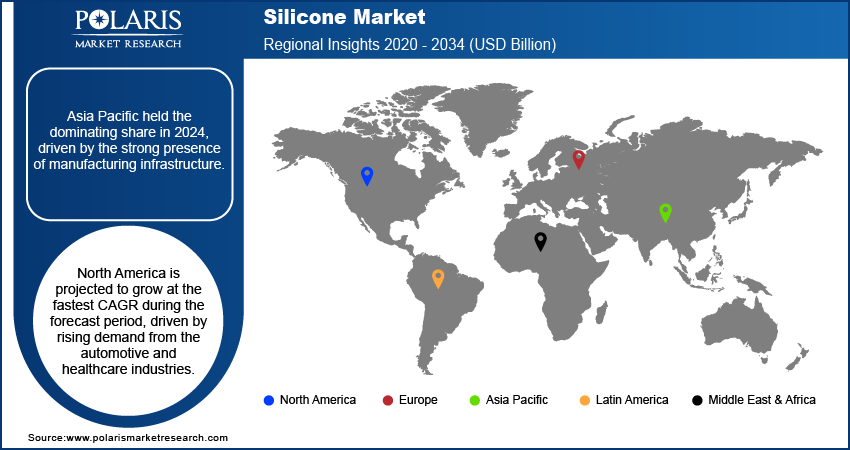

The global silicone market was valued at approximately USD 22.67 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of about 6.15% from 2025 through 2034. This expansion underscores the increasing strategic importance of silicones across geographic regions, particularly as regional manufacturing trends accelerate in North America, Europe and Asia Pacific. In North America the market is supported by the mature automotive and aerospace supply-base, strong regulatory frameworks for materials performance and established cross-border supply chains with Mexico and Canada. In Europe the interplay of sustainability regulation and infrastructure renewal programmes has strengthened demand for silicone-based sealants, coatings and insulation systems. In the Asia Pacific region rapid industrialisation, urbanisation and expanding electronics manufacturing hubs in China, India and Southeast Asia have contributed to robust growth in silicone demand, and this region is emerging as a pivotal manufacturing platform for global supply networks.

In North America the driver of demand is facilitated by high performance requirements for silicones in electric vehicle (EV) systems, renewable-energy installations and advanced HVAC applications. Regional manufacturing trends show that domestic resin and fluid production is increasingly integrated with site-specific development of silicone elastomers in the U.S., thereby strengthening supply-chain resilience. Meanwhile trade-specific factors such as tariffs on Chinese chemical imports and reshoring of silicone intermediates are influencing how multinationals manage their cross-border supply chains. In Europe the restraint of raw-material price volatility is partly moderated by tighter regional regulations on volatile organic compounds (VOCs) and polymer use, increasing demand for high-performance silicone alternatives. Market penetration strategies in Europe are also shifting toward premium silicone-based solutions in green construction and façade systems. Asia Pacific presents an opportunity-rich environment, with value chain optimisation playing a key role: local production of silicone fluids and elastomers is becoming cost-effective due to lower labour and operating costs, and aggressive expansion of electronics, personal-care and infrastructure fabrication is catalysing growth.

Drivers for the global silicone market across regions include increased demand in end-use application sectors such as automotive (including EVs), electronics & semiconductors, construction and personal care. For example, the adoption of silicone-based encapsulants and coatings in electronics manufacturing in Asia Pacific underscores application-specific growth and is compounded by the region’s rapid urbanisation and technology manufacturing clusters. Another driver is the push for more sustainable chemical platforms, where silicones are favoured for their weather-resistance, durability and performance stability. Restraints include the dependency on volatile raw materials such as chlorosilanes and the intensifying price competition among global suppliers, which can undermine margin stability. Furthermore, in regions with slower infrastructure investment (e.g., parts of Eastern Europe) market growth may lag, dampening the global aggregate.

Read More @ https://www.polarismarketresearch.com/industry-analysis/silicone-market

Opportunities lie in regional manufacturing footprint expansion: multinational silicone producers are establishing new plants in Asia Pacific and Latin America to cater to local demand while reducing logistics cost and lead-times. The ongoing shift in cross-border supply chains toward near-shoring of critical silicone intermediates offers manufacturers a chance to secure long-term competitiveness. In Europe, further opportunities exist in retro-fitting older buildings with silicone-based façades and sealants under national policy impact programmes aimed at improving energy efficiency. Trends also include consolidation of global supply chains, increased vertical integration by major players, and rising adoption of digitally-driven production platforms that boost yield and cut waste — all part of the broader thematic of value chain optimisation.

The global silicone market was valued at approximately USD 22.67 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of about 6.15% from 2025 through 2034. This expansion underscores the increasing strategic importance of silicones across geographic regions, particularly as regional manufacturing trends accelerate in North America, Europe and Asia Pacific. In North America the market is supported by the mature automotive and aerospace supply-base, strong regulatory frameworks for materials performance and established cross-border supply chains with Mexico and Canada. In Europe the interplay of sustainability regulation and infrastructure renewal programmes has strengthened demand for silicone-based sealants, coatings and insulation systems. In the Asia Pacific region rapid industrialisation, urbanisation and expanding electronics manufacturing hubs in China, India and Southeast Asia have contributed to robust growth in silicone demand, and this region is emerging as a pivotal manufacturing platform for global supply networks. In North America the driver of demand is facilitated by high performance requirements for silicones in electric vehicle (EV) systems, renewable-energy installations and advanced HVAC applications. Regional manufacturing trends show that domestic resin and fluid production is increasingly integrated with site-specific development of silicone elastomers in the U.S., thereby strengthening supply-chain resilience. Meanwhile trade-specific factors such as tariffs on Chinese chemical imports and reshoring of silicone intermediates are influencing how multinationals manage their cross-border supply chains. In Europe the restraint of raw-material price volatility is partly moderated by tighter regional regulations on volatile organic compounds (VOCs) and polymer use, increasing demand for high-performance silicone alternatives. Market penetration strategies in Europe are also shifting toward premium silicone-based solutions in green construction and façade systems. Asia Pacific presents an opportunity-rich environment, with value chain optimisation playing a key role: local production of silicone fluids and elastomers is becoming cost-effective due to lower labour and operating costs, and aggressive expansion of electronics, personal-care and infrastructure fabrication is catalysing growth. Drivers for the global silicone market across regions include increased demand in end-use application sectors such as automotive (including EVs), electronics & semiconductors, construction and personal care. For example, the adoption of silicone-based encapsulants and coatings in electronics manufacturing in Asia Pacific underscores application-specific growth and is compounded by the region’s rapid urbanisation and technology manufacturing clusters. Another driver is the push for more sustainable chemical platforms, where silicones are favoured for their weather-resistance, durability and performance stability. Restraints include the dependency on volatile raw materials such as chlorosilanes and the intensifying price competition among global suppliers, which can undermine margin stability. Furthermore, in regions with slower infrastructure investment (e.g., parts of Eastern Europe) market growth may lag, dampening the global aggregate. Read More @ https://www.polarismarketresearch.com/industry-analysis/silicone-market Opportunities lie in regional manufacturing footprint expansion: multinational silicone producers are establishing new plants in Asia Pacific and Latin America to cater to local demand while reducing logistics cost and lead-times. The ongoing shift in cross-border supply chains toward near-shoring of critical silicone intermediates offers manufacturers a chance to secure long-term competitiveness. In Europe, further opportunities exist in retro-fitting older buildings with silicone-based façades and sealants under national policy impact programmes aimed at improving energy efficiency. Trends also include consolidation of global supply chains, increased vertical integration by major players, and rising adoption of digitally-driven production platforms that boost yield and cut waste — all part of the broader thematic of value chain optimisation.0 Comentários 0 Compartilhamentos 920 Visualizações 0 Anterior -

Valued at USD 2.01 billion in 2024, the global smart home energy monitoring devices market is advancing at a CAGR of 16.91% through 2034, with growth increasingly segmented by product architecture, application scope, and integration depth. The market bifurcates into whole-home monitors and plug-in/circuit-level devices, with whole-home systems capturing 63% of revenue in 2024 due to their ability to provide granular appliance-level insights via machine learning algorithms that disaggregate energy signatures. Plug-in monitors, while cheaper (USD 25–50 vs. USD 200–400 for whole-home units), are losing share as consumers prioritize comprehensive visibility over point-of-use tracking. Within applications, residential dominates, but application-specific growth is accelerating in multi-family housing and prosumer solar+battery installations, where landlords and homeowners seek to verify system performance and optimize self-consumption.

Product differentiation has become a decisive competitive factor, particularly as hardware margins compress. Leaders now embed AI-driven forecasting, carbon intensity tracking (aligned with grid emission factors from sources like Electricity Maps), and automated load-shedding triggers—features that justify premium pricing and deepen user engagement. Segment-wise performance reveals clear stratification: DIY-installed monitors appeal to tech-savvy early adopters in North America, while professionally installed, utility-certified systems dominate in Europe due to regulatory requirements and rebate eligibility.

Read More @ https://www.polarismarketresearch.com/industry-analysis/smart-home-energy-monitoring-devices-market

Value chain optimization is critical in this capital-intensive segment; Emporia Energy’s vertical integration of current transformer (CT) sensor manufacturing and cloud analytics reduces BOM costs by 18%, per company filings, enabling aggressive pricing without sacrificing margins. Innovation is also reshaping form factors—non-invasive clamp-on sensors are giving way to DIN-rail mounted units with built-in cellular or Wi-Fi 6 connectivity, reducing installation complexity in retrofit scenarios. As utilities increasingly treat energy data as a service, segment leaders are shifting from one-time hardware sales to subscription models offering advanced analytics, anomaly alerts, and integration with time-of-use tariff optimization. This transition not only improves customer lifetime value but also aligns with the broader trend of software-defined energy management, where the device is merely the data gateway to a recurring revenue platform.

• Sense Labs, Inc.

• Emporia Energy

• Itron, Inc.

• Schneider Electric SE

• Aclara Technologies LLC

More Trending Latest Reports By Polaris Market Research:

Muscle Stimulator Market

Otoscope Market

Thermal Insulation Coating Market

HDPE Geogrid Market

Otoscope Market

Autonomous Port Operations Systems Market

DNA Synthesis Market

Autopilot System Market

Germany Medical Plastics Market

Valued at USD 2.01 billion in 2024, the global smart home energy monitoring devices market is advancing at a CAGR of 16.91% through 2034, with growth increasingly segmented by product architecture, application scope, and integration depth. The market bifurcates into whole-home monitors and plug-in/circuit-level devices, with whole-home systems capturing 63% of revenue in 2024 due to their ability to provide granular appliance-level insights via machine learning algorithms that disaggregate energy signatures. Plug-in monitors, while cheaper (USD 25–50 vs. USD 200–400 for whole-home units), are losing share as consumers prioritize comprehensive visibility over point-of-use tracking. Within applications, residential dominates, but application-specific growth is accelerating in multi-family housing and prosumer solar+battery installations, where landlords and homeowners seek to verify system performance and optimize self-consumption. Product differentiation has become a decisive competitive factor, particularly as hardware margins compress. Leaders now embed AI-driven forecasting, carbon intensity tracking (aligned with grid emission factors from sources like Electricity Maps), and automated load-shedding triggers—features that justify premium pricing and deepen user engagement. Segment-wise performance reveals clear stratification: DIY-installed monitors appeal to tech-savvy early adopters in North America, while professionally installed, utility-certified systems dominate in Europe due to regulatory requirements and rebate eligibility. Read More @ https://www.polarismarketresearch.com/industry-analysis/smart-home-energy-monitoring-devices-market Value chain optimization is critical in this capital-intensive segment; Emporia Energy’s vertical integration of current transformer (CT) sensor manufacturing and cloud analytics reduces BOM costs by 18%, per company filings, enabling aggressive pricing without sacrificing margins. Innovation is also reshaping form factors—non-invasive clamp-on sensors are giving way to DIN-rail mounted units with built-in cellular or Wi-Fi 6 connectivity, reducing installation complexity in retrofit scenarios. As utilities increasingly treat energy data as a service, segment leaders are shifting from one-time hardware sales to subscription models offering advanced analytics, anomaly alerts, and integration with time-of-use tariff optimization. This transition not only improves customer lifetime value but also aligns with the broader trend of software-defined energy management, where the device is merely the data gateway to a recurring revenue platform. • Sense Labs, Inc. • Emporia Energy • Itron, Inc. • Schneider Electric SE • Aclara Technologies LLC More Trending Latest Reports By Polaris Market Research: Muscle Stimulator Market Otoscope Market Thermal Insulation Coating Market HDPE Geogrid Market Otoscope Market Autonomous Port Operations Systems Market DNA Synthesis Market Autopilot System Market Germany Medical Plastics Market0 Comentários 0 Compartilhamentos 782 Visualizações 0 Anterior -

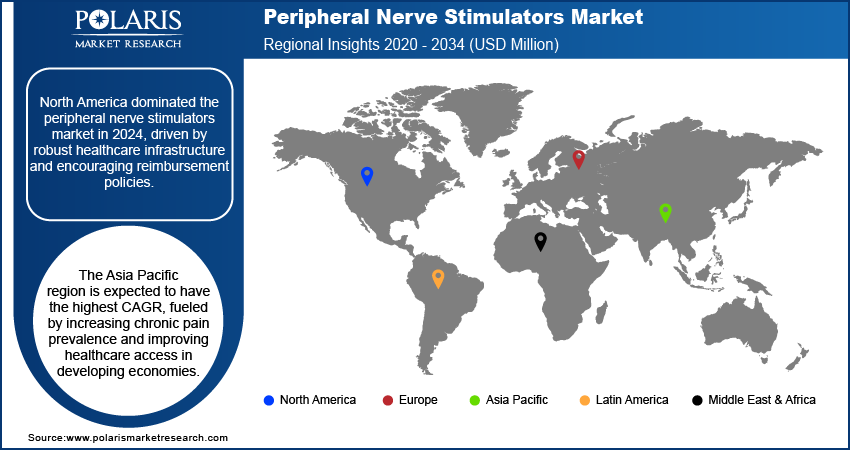

The global peripheral nerve stimulators market was valued at USD 607.31 million in 2024 and is projected to grow at a CAGR of 4.81% from 2025-2032. This segmentation-driven perspective reveals that not all parts of the market will grow equally: product differentiation, application-specific growth, value-chain optimisation and segment-wise performance will determine winners. Key segments include device type (transcutaneous, percutaneous, implantable), end-user setting (hospitals, outpatient centres, home-based therapy) and application (chronic pain, neuropathy, post-surgical nerve damage). Understanding the segmentation is critical for market participants as price-points, adoption rates and service-models vary significantly across each.

Product differentiation is increasingly important: for example transcutaneous peripheral nerve stimulators (non-invasive) typically command higher adoption in outpatient and home-therapy settings due to ease of use and minimal invasive risk, while implantable devices carry greater cost and more stringent regulatory demands but may yield higher margins. Application-specific growth is evident in neuropathic pain and post-surgical nerve injury segments where adoption is growing, versus more established chronic-pain segments where replacement cycles between devices are longer. Value-chain optimisation is visible as manufacturers increasingly bundle device sales with remote-monitoring software, clinician-training modules, and service-contracts, shifting from a pure hardware-sale model to a “device-plus-service” model. Segment-wise performance shows that while hospital-based device adoption remains largest in revenue, the fastest-growing unit segment is outpatient and home-based therapies where convenience and non-invasive formats reduce total cost of ownership.