The global carbon fiber market reached a valuation of USD 8.81 billion in 2024 and is anticipated to grow at a CAGR of 12.9% from 2025 to 2034, propelled by rising demand across diversified product categories and end-user sectors. The segmentation of this market by product type, application, and end-use industries provides a comprehensive view of how product differentiation and segment-wise performance are shaping global growth. Strategic value chain optimization has become central to the competitive outlook, with innovations targeting enhanced performance and reduced production costs.

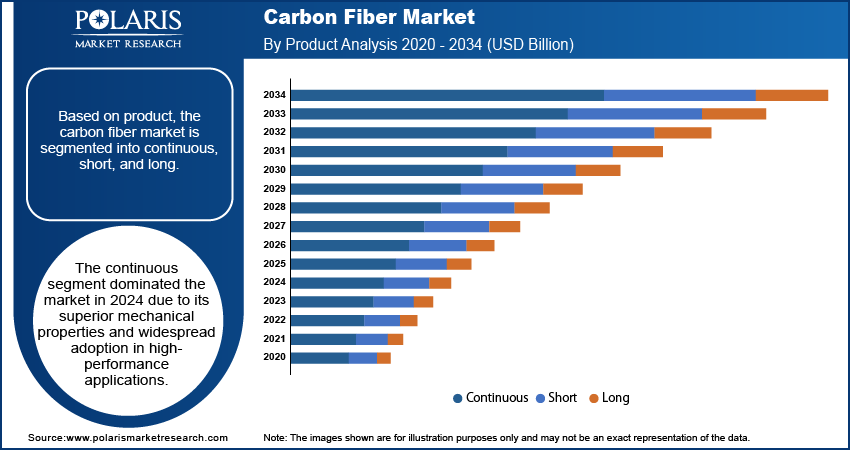

By product type, the market is segmented into PAN-based carbon fiber, pitch-based carbon fiber, and rayon-based variants. PAN-based carbon fiber dominates due to its high tensile strength and wide usage across aerospace, automotive, and energy applications. The cost-performance balance of PAN-based products drives large-scale adoption, particularly in applications where durability and strength-to-weight ratio are critical. Pitch-based carbon fibers, while costlier, are gaining traction in niche applications such as aerospace and thermal management solutions, valued for their high modulus properties. Rayon-based fibers represent a smaller share but are being revived through R&D advancements focused on sustainable production techniques.

Application-specific growth highlights the significance of aerospace and defense as the largest demand driver, where carbon fiber composites are essential for structural performance and weight reduction. The International Air Transport Association (IATA) projects rising aircraft deliveries, which in turn accelerates demand for carbon fiber materials in fuselage and wing structures. The automotive sector is the fastest-growing application, with manufacturers incorporating composites into electric vehicles to improve battery efficiency and extend driving range. Wind energy also represents a robust growth segment, with the International Energy Agency (IEA) emphasizing expanded turbine blade sizes that require stronger and lighter materials. Sports equipment, infrastructure, and industrial applications add further diversification to the demand landscape.

End-user segmentation underscores the prominence of aerospace manufacturers, automotive OEMs, renewable energy firms, and industrial producers. Aerospace remains the largest revenue contributor, supported by defense contracts and increasing commercial aircraft production. Automotive companies are scaling adoption through partnerships with carbon fiber manufacturers, integrating lightweight materials into chassis and body panels. Renewable energy providers are investing in longer and more durable turbine blades, highlighting application-specific growth potential. Industrial sectors, including oil and gas and civil engineering, utilize carbon fiber composites for corrosion resistance and durability, expanding the sector’s relevance beyond traditional markets.

Read More @ https://www.polarismarketresearch.com/industry-analysis/carbon-fiber-market

Market dynamics reflect strong drivers such as sustainability policies, lightweighting imperatives, and rising energy transition investments. Restraints remain in the form of high manufacturing costs and recycling challenges, although technological advancements in thermoplastic composites are mitigating these limitations. Opportunities exist in tailoring solutions for value chain optimization, particularly through scalable and cost-effective production. Trends include automation in carbon fiber layup, increasing adoption of recycled fibers, and hybrid composite structures for advanced functionality.

The competitive landscape is led by companies that have invested heavily in R&D, product differentiation, and global distribution. Their ability to optimize segment-wise performance across end-use industries consolidates their leadership. Leading players with significant market presence include:

• Toray Industries

• Mitsubishi Chemical Carbon Fiber and Composites

• Teijin Limited

• Hexcel Corporation

• SGL Carbon

With demand growth diversified across multiple segments, the carbon fiber market is poised for strong expansion, supported by product differentiation strategies and deep integration into industrial value chains worldwide.

By product type, the market is segmented into PAN-based carbon fiber, pitch-based carbon fiber, and rayon-based variants. PAN-based carbon fiber dominates due to its high tensile strength and wide usage across aerospace, automotive, and energy applications. The cost-performance balance of PAN-based products drives large-scale adoption, particularly in applications where durability and strength-to-weight ratio are critical. Pitch-based carbon fibers, while costlier, are gaining traction in niche applications such as aerospace and thermal management solutions, valued for their high modulus properties. Rayon-based fibers represent a smaller share but are being revived through R&D advancements focused on sustainable production techniques.

Application-specific growth highlights the significance of aerospace and defense as the largest demand driver, where carbon fiber composites are essential for structural performance and weight reduction. The International Air Transport Association (IATA) projects rising aircraft deliveries, which in turn accelerates demand for carbon fiber materials in fuselage and wing structures. The automotive sector is the fastest-growing application, with manufacturers incorporating composites into electric vehicles to improve battery efficiency and extend driving range. Wind energy also represents a robust growth segment, with the International Energy Agency (IEA) emphasizing expanded turbine blade sizes that require stronger and lighter materials. Sports equipment, infrastructure, and industrial applications add further diversification to the demand landscape.

End-user segmentation underscores the prominence of aerospace manufacturers, automotive OEMs, renewable energy firms, and industrial producers. Aerospace remains the largest revenue contributor, supported by defense contracts and increasing commercial aircraft production. Automotive companies are scaling adoption through partnerships with carbon fiber manufacturers, integrating lightweight materials into chassis and body panels. Renewable energy providers are investing in longer and more durable turbine blades, highlighting application-specific growth potential. Industrial sectors, including oil and gas and civil engineering, utilize carbon fiber composites for corrosion resistance and durability, expanding the sector’s relevance beyond traditional markets.

Read More @ https://www.polarismarketresearch.com/industry-analysis/carbon-fiber-market

Market dynamics reflect strong drivers such as sustainability policies, lightweighting imperatives, and rising energy transition investments. Restraints remain in the form of high manufacturing costs and recycling challenges, although technological advancements in thermoplastic composites are mitigating these limitations. Opportunities exist in tailoring solutions for value chain optimization, particularly through scalable and cost-effective production. Trends include automation in carbon fiber layup, increasing adoption of recycled fibers, and hybrid composite structures for advanced functionality.

The competitive landscape is led by companies that have invested heavily in R&D, product differentiation, and global distribution. Their ability to optimize segment-wise performance across end-use industries consolidates their leadership. Leading players with significant market presence include:

• Toray Industries

• Mitsubishi Chemical Carbon Fiber and Composites

• Teijin Limited

• Hexcel Corporation

• SGL Carbon

With demand growth diversified across multiple segments, the carbon fiber market is poised for strong expansion, supported by product differentiation strategies and deep integration into industrial value chains worldwide.

The global carbon fiber market reached a valuation of USD 8.81 billion in 2024 and is anticipated to grow at a CAGR of 12.9% from 2025 to 2034, propelled by rising demand across diversified product categories and end-user sectors. The segmentation of this market by product type, application, and end-use industries provides a comprehensive view of how product differentiation and segment-wise performance are shaping global growth. Strategic value chain optimization has become central to the competitive outlook, with innovations targeting enhanced performance and reduced production costs.

By product type, the market is segmented into PAN-based carbon fiber, pitch-based carbon fiber, and rayon-based variants. PAN-based carbon fiber dominates due to its high tensile strength and wide usage across aerospace, automotive, and energy applications. The cost-performance balance of PAN-based products drives large-scale adoption, particularly in applications where durability and strength-to-weight ratio are critical. Pitch-based carbon fibers, while costlier, are gaining traction in niche applications such as aerospace and thermal management solutions, valued for their high modulus properties. Rayon-based fibers represent a smaller share but are being revived through R&D advancements focused on sustainable production techniques.

Application-specific growth highlights the significance of aerospace and defense as the largest demand driver, where carbon fiber composites are essential for structural performance and weight reduction. The International Air Transport Association (IATA) projects rising aircraft deliveries, which in turn accelerates demand for carbon fiber materials in fuselage and wing structures. The automotive sector is the fastest-growing application, with manufacturers incorporating composites into electric vehicles to improve battery efficiency and extend driving range. Wind energy also represents a robust growth segment, with the International Energy Agency (IEA) emphasizing expanded turbine blade sizes that require stronger and lighter materials. Sports equipment, infrastructure, and industrial applications add further diversification to the demand landscape.

End-user segmentation underscores the prominence of aerospace manufacturers, automotive OEMs, renewable energy firms, and industrial producers. Aerospace remains the largest revenue contributor, supported by defense contracts and increasing commercial aircraft production. Automotive companies are scaling adoption through partnerships with carbon fiber manufacturers, integrating lightweight materials into chassis and body panels. Renewable energy providers are investing in longer and more durable turbine blades, highlighting application-specific growth potential. Industrial sectors, including oil and gas and civil engineering, utilize carbon fiber composites for corrosion resistance and durability, expanding the sector’s relevance beyond traditional markets.

Read More @ https://www.polarismarketresearch.com/industry-analysis/carbon-fiber-market

Market dynamics reflect strong drivers such as sustainability policies, lightweighting imperatives, and rising energy transition investments. Restraints remain in the form of high manufacturing costs and recycling challenges, although technological advancements in thermoplastic composites are mitigating these limitations. Opportunities exist in tailoring solutions for value chain optimization, particularly through scalable and cost-effective production. Trends include automation in carbon fiber layup, increasing adoption of recycled fibers, and hybrid composite structures for advanced functionality.

The competitive landscape is led by companies that have invested heavily in R&D, product differentiation, and global distribution. Their ability to optimize segment-wise performance across end-use industries consolidates their leadership. Leading players with significant market presence include:

• Toray Industries

• Mitsubishi Chemical Carbon Fiber and Composites

• Teijin Limited

• Hexcel Corporation

• SGL Carbon

With demand growth diversified across multiple segments, the carbon fiber market is poised for strong expansion, supported by product differentiation strategies and deep integration into industrial value chains worldwide.

0 Commentaires

0 Parts

1KB Vue

0 Aperçu