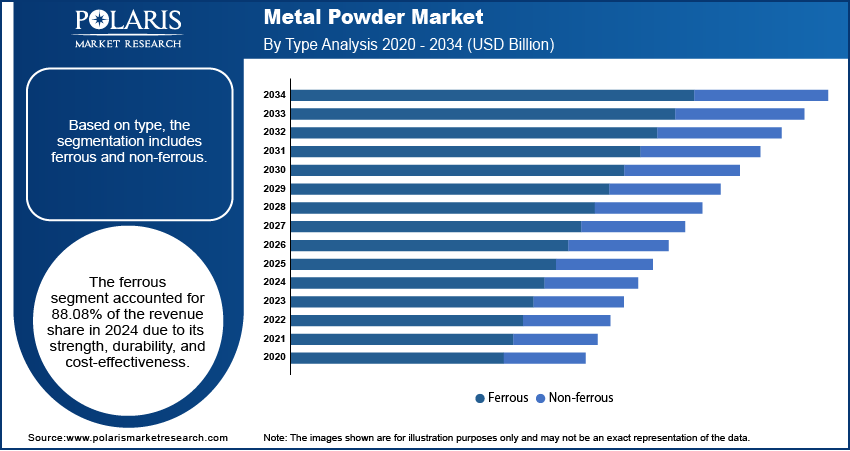

The global metal powder market size was valued at USD 6.10 billion in 2024 and is projected to expand at a CAGR of 7.01 % from 2025 to 2034, reflecting accelerating demand across additive manufacturing, powder metallurgy, and specialty alloys. In this accelerating environment, regional manufacturing trends, cross-border supply chains, and market penetration strategies will decide which geographies lead in supply, innovation, and adoption. Firms must navigate shifting trade policies, regulatory norms, and technological leadership to secure long-term positioning.

In Asia Pacific, the metal powder market already commands a dominant share globally. Precedence Research reports Asia Pacific held roughly 35 % of the global market in 2024, driven by large-scale electronics, automotive, aerospace, and industrial manufacturing bases in China, Japan, South Korea, and Southeast Asia.Regional manufacturing trends in Asia are skewed toward vertical integration—metal powder producers are increasingly establishing downstream additive manufacturing or powder metallurgy units to capture more of the value chain. Cross-border supply chains from China into North America and Europe remain robust, though periodic raw material export controls and freight cost volatility introduce risk. In North America, strong aerospace demand, defense procurement, and adoption of metal 3D printing drive localized demand. However, trade-specific factors—such as import duties on specialty powders or rare metal inputs—force many North American operators to source from allied geographies or ramp local capacity. In Europe, there is a strong push for reshoring and supply chain resilience. European manufacturers often adopt regional penetration strategies by locating powder production closer to key end-user hubs (Germany, France, Italy). Regulatory frameworks such as REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) and stringent environmental controls favor powder producers who localize or co-manufacture within the EU to minimize cross-border regulatory friction.

Analyzing core market dynamics, Drivers include the rapid adoption of additive manufacturing (AM) across aerospace, medical, and automotive sectors, the demand for lightweight and complex components, and the need for novel alloy powders (e.g. titanium, nickel, cobalt, aluminum) that meet performance requirements. The broader push for electrification of mobility and lightweighting in EVs intensifies demand for powder-based components in motors, battery housings, and structural parts. The Business Research Company highlights that electric vehicle demand is a key growth catalyst for the metal powder market.Restraints include high raw material costs (especially for critical or rare metals), challenges in achieving consistent particle size distribution and purity at scale, and capital intensity of powder atomization and classification plants. In many regions, regulatory or environmental constraints on metal powder emissions, dust control, and hazardous substance handling impose additional cost. Global supply bottlenecks in specialty metals (e.g. rare earths, nickel alloys) further restrain full-scale expansion.

Read More @

https://www.polarismarketresearch.com/industry-analysis/metal-powder-market

Opportunities lie in regional capacity expansion, alloy innovation, backward integration, and servicing localized demand. In Asia Pacific, firms can invest in downstream AM or metal injection molding (MIM) plants near powder production sites to reduce logistics and enhance margin capture. In North America and Europe, supply resilience and nearshoring represent opportunities—powder manufacturers can locate near aerospace, defense, or industrial clusters to reduce lead time and trade risk. Developing next-generation alloy powders optimized for additive manufacturing or hybrid manufacturing (powder + subtractive) provides differentiation opportunity. Manufacturers can also pursue value chain optimization by integrating powder production, classification, and finishing operations, reducing cost and improving yield. Sourcing feedstock metal powder scrap or recycled metals as feed for powder processes offers circularity value and raw material hedging.

Trends shaping future dynamics include consolidation among powder producers as firms scale to meet CAPEX needs and competitive pressures. Second, regional modular plants—smaller, agile atomization or classification lines placed near end users—emerge to reduce transportation costs and buffer against supply chain disruption. Third, application-driven alloy development deepens: customized powders matched to specific AM or MIM processes will become more common,

The global metal powder market size was valued at USD 6.10 billion in 2024 and is projected to expand at a CAGR of 7.01 % from 2025 to 2034, reflecting accelerating demand across additive manufacturing, powder metallurgy, and specialty alloys. In this accelerating environment, regional manufacturing trends, cross-border supply chains, and market penetration strategies will decide which geographies lead in supply, innovation, and adoption. Firms must navigate shifting trade policies, regulatory norms, and technological leadership to secure long-term positioning.

In Asia Pacific, the metal powder market already commands a dominant share globally. Precedence Research reports Asia Pacific held roughly 35 % of the global market in 2024, driven by large-scale electronics, automotive, aerospace, and industrial manufacturing bases in China, Japan, South Korea, and Southeast Asia.Regional manufacturing trends in Asia are skewed toward vertical integration—metal powder producers are increasingly establishing downstream additive manufacturing or powder metallurgy units to capture more of the value chain. Cross-border supply chains from China into North America and Europe remain robust, though periodic raw material export controls and freight cost volatility introduce risk. In North America, strong aerospace demand, defense procurement, and adoption of metal 3D printing drive localized demand. However, trade-specific factors—such as import duties on specialty powders or rare metal inputs—force many North American operators to source from allied geographies or ramp local capacity. In Europe, there is a strong push for reshoring and supply chain resilience. European manufacturers often adopt regional penetration strategies by locating powder production closer to key end-user hubs (Germany, France, Italy). Regulatory frameworks such as REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) and stringent environmental controls favor powder producers who localize or co-manufacture within the EU to minimize cross-border regulatory friction.

Analyzing core market dynamics, Drivers include the rapid adoption of additive manufacturing (AM) across aerospace, medical, and automotive sectors, the demand for lightweight and complex components, and the need for novel alloy powders (e.g. titanium, nickel, cobalt, aluminum) that meet performance requirements. The broader push for electrification of mobility and lightweighting in EVs intensifies demand for powder-based components in motors, battery housings, and structural parts. The Business Research Company highlights that electric vehicle demand is a key growth catalyst for the metal powder market.Restraints include high raw material costs (especially for critical or rare metals), challenges in achieving consistent particle size distribution and purity at scale, and capital intensity of powder atomization and classification plants. In many regions, regulatory or environmental constraints on metal powder emissions, dust control, and hazardous substance handling impose additional cost. Global supply bottlenecks in specialty metals (e.g. rare earths, nickel alloys) further restrain full-scale expansion.

Read More @ https://www.polarismarketresearch.com/industry-analysis/metal-powder-market

Opportunities lie in regional capacity expansion, alloy innovation, backward integration, and servicing localized demand. In Asia Pacific, firms can invest in downstream AM or metal injection molding (MIM) plants near powder production sites to reduce logistics and enhance margin capture. In North America and Europe, supply resilience and nearshoring represent opportunities—powder manufacturers can locate near aerospace, defense, or industrial clusters to reduce lead time and trade risk. Developing next-generation alloy powders optimized for additive manufacturing or hybrid manufacturing (powder + subtractive) provides differentiation opportunity. Manufacturers can also pursue value chain optimization by integrating powder production, classification, and finishing operations, reducing cost and improving yield. Sourcing feedstock metal powder scrap or recycled metals as feed for powder processes offers circularity value and raw material hedging.

Trends shaping future dynamics include consolidation among powder producers as firms scale to meet CAPEX needs and competitive pressures. Second, regional modular plants—smaller, agile atomization or classification lines placed near end users—emerge to reduce transportation costs and buffer against supply chain disruption. Third, application-driven alloy development deepens: customized powders matched to specific AM or MIM processes will become more common,