DevSecOps Market Size, Trends, and Strategic Insights 2026–2033

Market Size and Overview

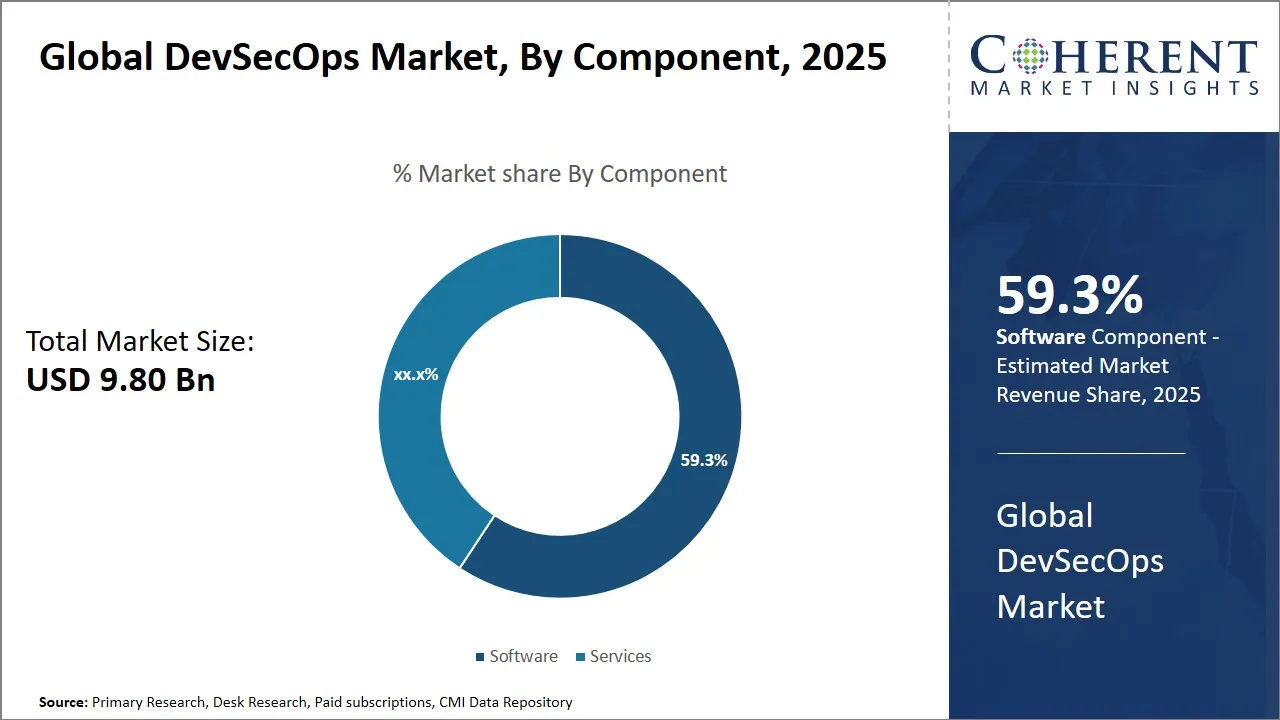

The Global Devsecops Market is estimated to be valued at USD 9.80 Bn in 2026 and is expected to reach USD 27.6 Bn by 2033, exhibiting a compound annual growth rate (CAGR) of 12.8% from 2026 to 2033.

https://www.coherentmarketinsights.com/industry-reports/devsecops-market

IT and Telecom, BFSI, Government, Retail and Consumer Goods, Manufacturing,Coherent Market Insights , DevSecOps Market , DevSecOps Market Growth , DevSecOps Market Reports,

Market Size and Overview

The Global Devsecops Market is estimated to be valued at USD 9.80 Bn in 2026 and is expected to reach USD 27.6 Bn by 2033, exhibiting a compound annual growth rate (CAGR) of 12.8% from 2026 to 2033.

https://www.coherentmarketinsights.com/industry-reports/devsecops-market

IT and Telecom, BFSI, Government, Retail and Consumer Goods, Manufacturing,Coherent Market Insights , DevSecOps Market , DevSecOps Market Growth , DevSecOps Market Reports,

DevSecOps Market Size, Trends, and Strategic Insights 2026–2033

Market Size and Overview

The Global Devsecops Market is estimated to be valued at USD 9.80 Bn in 2026 and is expected to reach USD 27.6 Bn by 2033, exhibiting a compound annual growth rate (CAGR) of 12.8% from 2026 to 2033.

https://www.coherentmarketinsights.com/industry-reports/devsecops-market

IT and Telecom, BFSI, Government, Retail and Consumer Goods, Manufacturing,Coherent Market Insights , DevSecOps Market , DevSecOps Market Growth , DevSecOps Market Reports,

0 Commentarii

0 Distribuiri

63 Views

0 previzualizare