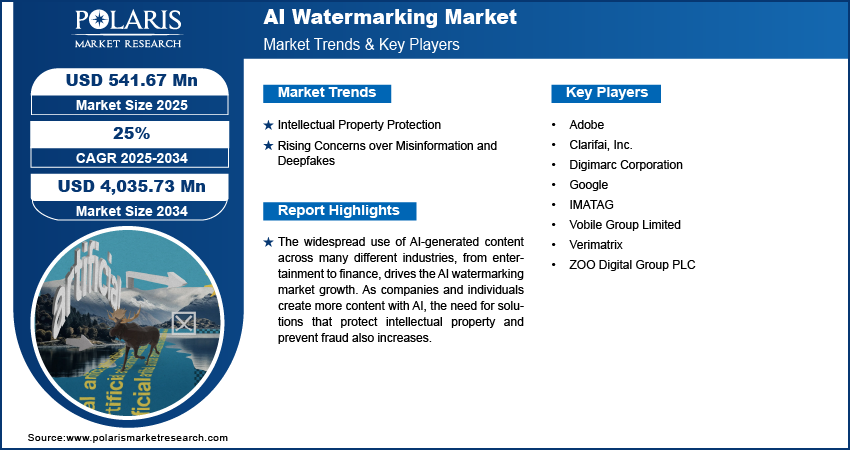

The global AI watermarking market size was valued at USD 434.20 million in 2024 and is anticipated to register a CAGR of 25 % from 2025 to 2034. This trajectory reflects rapid adoption of provenance, traceability, and authenticity tools amidst proliferation of generative AI, user content platforms, and regulation around disinformation. While North America leads in absolute investment and ecosystem maturity, Asia Pacific is emerging as the highest-growth frontier, and Europe must contend with nuanced regulation and data sovereignty constraints. The regional dynamics of manufacturing, cross-border supply chains, and market penetration strategies will be critical to which vendors scale fastest and lock in durable moats.

In North America, the U.S. and Canada drive demand for AI watermarking primarily from their dense technology, media, entertainment, and platform economy ecosystems. Leading content platforms, cloud service providers, and AI labs push watermarking into standards and operational pipelines to preempt misuse of generative content. The U.S. institutional funding, venture capital flows, and strong IP regimes incentivize watermarking R&D and adoption. At the same time, supply chains for watermarking infrastructure (server clusters, specialized cryptographic modules, and encryption hardware) often draw on cross-border technology suppliers; recent restrictions on certain cryptographic exports or semiconductors may force regional manufacturing trends to localize watermarking hardware or encryption modules.

In Asia Pacific, particularly in China, India, Japan, and South Korea, digital transformation, AI adoption, and mobile content proliferation are fueling watermarking uptake at high rates. According to one market report, Asia Pacific is emerging as the fastest-growing region in the AI watermarking market.The Chinese digital policy emphasis on content provenance, censorship, and regulation of AI content means local watermarking standards and compliance modules may diverge from global norms. Indian and Southeast Asian regulators likewise begin exploring mandates for content origin verification. Cross-border data flows, localization rules, and export of watermarking algorithms become friction points in supply chains and in vendor global rollout strategies. Thus, market penetration strategies in APAC often rely on joint ventures, on-shore deployment, and co-development with local cloud and telecom providers.

In Europe, regulatory complexity is a significant moderating factor. The EU’s Digital Services Act, proposed AI Act, and emerging rules on deepfake transparency push watermarking into compliance toolkits. But data protection regimes, national digital sovereignty, and cross-border GDPR requirements force watermarking vendors to tailor regional orchestration nodes, local key management, and differ integration by country. In particular, European customers may demand localized watermark anchors or cryptographic modules that don’t route through non-EU servers. This increases deployment complexity and potentially slows real adoption. Still, Europe's strong creative and media production industries, combined with unified regulation trends, form a substantial addressable base.

Drivers across these regions stem from the explosion of generative content (images, video, text), increasing concerns about deepfake, misinformation and IP infringement, and regulatory momentum toward content authenticity mandates. The ITU and other standards bodies have underscored AI watermarking as critical to multimedia authenticity. ITU The more that platforms, publishers, and governments demand provenance, the stronger the pull. In North America, ecosystem readiness, capital flows, and early standards formation further accelerate uptake. In APAC, surging digital content volumes and regulatory push amplify growth. Europe’s driver is partially regulatory pressure, partially demand from media and adtech sectors needing robust anti-piracy watermarking.

Restraints include interoperability challenges, fragmentation of watermarking standards, computational overhead (especially for real-time or streaming watermark embedding), resistance from content creators wary of perceptual artifacts, and competitive tensions with alternative authenticity systems (cryptographic signatures, metadata provenance). In Asia, limitations in computational infrastructure or encryption export regimes can hamper seamless deployment. In Europe, strict regulation or privacy constraints may inhibit watermarking in certain sensitive streams (health, biometrics). Further, scaling watermarking across billions of content objects imposes backend cost pressures.

Read More @

https://www.polarismarketresearch.com/industry-analysis/ai-watermarking-market

The global AI watermarking market size was valued at USD 434.20 million in 2024 and is anticipated to register a CAGR of 25 % from 2025 to 2034. This trajectory reflects rapid adoption of provenance, traceability, and authenticity tools amidst proliferation of generative AI, user content platforms, and regulation around disinformation. While North America leads in absolute investment and ecosystem maturity, Asia Pacific is emerging as the highest-growth frontier, and Europe must contend with nuanced regulation and data sovereignty constraints. The regional dynamics of manufacturing, cross-border supply chains, and market penetration strategies will be critical to which vendors scale fastest and lock in durable moats.

In North America, the U.S. and Canada drive demand for AI watermarking primarily from their dense technology, media, entertainment, and platform economy ecosystems. Leading content platforms, cloud service providers, and AI labs push watermarking into standards and operational pipelines to preempt misuse of generative content. The U.S. institutional funding, venture capital flows, and strong IP regimes incentivize watermarking R&D and adoption. At the same time, supply chains for watermarking infrastructure (server clusters, specialized cryptographic modules, and encryption hardware) often draw on cross-border technology suppliers; recent restrictions on certain cryptographic exports or semiconductors may force regional manufacturing trends to localize watermarking hardware or encryption modules.

In Asia Pacific, particularly in China, India, Japan, and South Korea, digital transformation, AI adoption, and mobile content proliferation are fueling watermarking uptake at high rates. According to one market report, Asia Pacific is emerging as the fastest-growing region in the AI watermarking market.The Chinese digital policy emphasis on content provenance, censorship, and regulation of AI content means local watermarking standards and compliance modules may diverge from global norms. Indian and Southeast Asian regulators likewise begin exploring mandates for content origin verification. Cross-border data flows, localization rules, and export of watermarking algorithms become friction points in supply chains and in vendor global rollout strategies. Thus, market penetration strategies in APAC often rely on joint ventures, on-shore deployment, and co-development with local cloud and telecom providers.

In Europe, regulatory complexity is a significant moderating factor. The EU’s Digital Services Act, proposed AI Act, and emerging rules on deepfake transparency push watermarking into compliance toolkits. But data protection regimes, national digital sovereignty, and cross-border GDPR requirements force watermarking vendors to tailor regional orchestration nodes, local key management, and differ integration by country. In particular, European customers may demand localized watermark anchors or cryptographic modules that don’t route through non-EU servers. This increases deployment complexity and potentially slows real adoption. Still, Europe's strong creative and media production industries, combined with unified regulation trends, form a substantial addressable base.

Drivers across these regions stem from the explosion of generative content (images, video, text), increasing concerns about deepfake, misinformation and IP infringement, and regulatory momentum toward content authenticity mandates. The ITU and other standards bodies have underscored AI watermarking as critical to multimedia authenticity. ITU The more that platforms, publishers, and governments demand provenance, the stronger the pull. In North America, ecosystem readiness, capital flows, and early standards formation further accelerate uptake. In APAC, surging digital content volumes and regulatory push amplify growth. Europe’s driver is partially regulatory pressure, partially demand from media and adtech sectors needing robust anti-piracy watermarking.

Restraints include interoperability challenges, fragmentation of watermarking standards, computational overhead (especially for real-time or streaming watermark embedding), resistance from content creators wary of perceptual artifacts, and competitive tensions with alternative authenticity systems (cryptographic signatures, metadata provenance). In Asia, limitations in computational infrastructure or encryption export regimes can hamper seamless deployment. In Europe, strict regulation or privacy constraints may inhibit watermarking in certain sensitive streams (health, biometrics). Further, scaling watermarking across billions of content objects imposes backend cost pressures.

Read More @ https://www.polarismarketresearch.com/industry-analysis/ai-watermarking-market

-market-by-end-use-analysis,-2020---2034.webp)